New funding for microenterprises and SMEs

Already before COVID-19, youth unemployment was high in Sweden, and large parts of the potential workforce was entirely dependent on social benefits. Better access to new forms of funding for microenterprises and SMEs, would be particularly helpful for these groups. The crisis will make the situation worse, but will it also be an opportunity to turn the development around?

Pontus Engström, Sofia Altafi, Gabriel Karlberg, and Sophie Nachemson-Ekvall

COVID-19 makes the struggle for jobs worse

The ongoing COVID-19 pandemic has far-reaching consequences for entrepreneurship and the ability of people to generate an income. Even before the pandemic, the struggle and competition for jobs in Europe as well as in Sweden was intensifying and inequality along with segregation was on the rise. Especially vulnerable and marginalized groups on the labor market include refugees and migrants but also youth. In Sweden, over 13% of the potential workforce lived entirely on social benefits before the COVID-19 outbreak. The Swedish welfare model, which is built on the idea of high involvement and high degree of employment in the population, is currently seeing Europe‘s highest employment gap between domestic born and foreign born. Youth unemployment in Sweden was 20% in 2019, which compares to 11% in Denmark and 10% in Norway. In a Swedish context, where large groups are excluded from the labor market, the entire basis of social capital will risk start eroding, leading to a society of mistrust and alienation.

The Swedish model has historically been built on the idea of large corporations and strong unions working together in one of the world’s tightest corporative arrangements, while microenterprises in particular but also SMEs have to a large extent been neglected by both the traditional market actors and the policy makers. From a historical and development perspective the uneven focus is understandable, but often pointed out as a risk factor by economists. In a global context, Sweden has been a leading force in both international aid and environmental matters, not the least through climate activist Greta Thunberg. While Sweden has internationally had a strong ambition of fulfilling the 17 UN Sustainable Development Goals (SDGs), through governmental agencies like Swedish International Development Cooperation Agency (Sida), the same focus cannot be said to have been the case domestically.

The tendency of neglecting deteriorating social issues in society is a sign of declining social capital, but the COVID-19 outbreak puts social capital back on everyone’s agenda. Rightly handled, a number of different policy instruments could be introduced to deal with the crisis and simultaneously be canalized into new initiatives designed to strengthen social cohesion.

The welfare offering, streamlined to suit the classical Swedish labor market model, proved ill-adapted to cope with the multi-faceted needs from a new generation of non-European migrants. The COVID-19 outbreak poses new challenges to the quality of the general quality of the welfare service, which in Sweden is highly dependent on personal income tax. With an expected increase in the unemployment rate, fewer taxpayers will need to bear a larger share of the burden. Businesses of all sizes are being affected. With a shrinking global market, and the need for a stronger domestic focus, the need for a conducive environment for small and medium-sized enterprises (SMEs) and microenterprises is high.

We lay out the foundation for a more inclusive financing of microenterprises and SMEs. It should not only be easier for SMEs to hire more people, but they should also be encouraged to activate the large already existing vulnerable segment of the population who even before the COVID-19 outbreak were excluded from formal job opportunities. We propose a combination of policy instruments, specifically the introduction of a new microfinance initiative, backed by government guarantees, in combination with business training and an active support from actors across society, including civil society and other hybrid organizations.

Accelerating unemployment of foreign born, especially women

A recent report by the Swedish Entrepreneurship Forum3 indicates that as many as 772 000 individuals, or 13.3% of the Swedish work force, were living completely on social benefits. Recent research shows that it takes 12-13 years for 50% of the group defined as foreign-born to obtain a subsistence level in Sweden. While the unemployment rate was 3.8% in the whole population, a staggering 15.8% rate is reported for the foreign-born segment – with women in particular being left out. Thus, Sweden becomes the country with the highest employment gap between foreign and domestic born in all of Europe. In addition, the Swedish youth unemployment rate – at 21% in 2020 and increasing, remains at the higher end of the countries.

The proportion of the population born in a non-European country and either registered as unemployed with the Swedish employment service or active in public-sponsored support programs has increased from 10% in the early 2000s to over 50%. While economists have pointed out this development for years, it may be that the COVID-19 pandemic now creates the necessary catalyst for change. A number of supportive packages have been presented as a way to mitigate the economic consequences of the crisis, including loans and credit guarantees to the commercial sector, the export industries as well as family firms. Different unemployment benefit-programs have been generously implemented, also aimed at citizens without full-time employment.

Although the very large and mostly export-oriented corporations still constitute a significant force in society as they account for 40% of the total sales and value added, two thirds of employees in the private sector, about 3.5 million people, work in microenterprises or SMEs. With many expected layoffs, increased global protectionism and lessened dependence on global growth as a result of the COVID-19 crisis, in Sweden we will see an increased reliance on jobs dependent on the domestic market. This challenges the Swedish corporatist model on the labor market in two ways. Firstly, traditional layoffs of full-time workers and the retraining and re-employment in new and growing export industries is less likely to be successful. Secondly, both the private and public segments of the infrastructure in Sweden are catering to large and export-oriented corporations, leaving microenterprises and SMEs in a comparatively disadvantaged situation.

The COVID-19 pandemic is unprecedented in modern times, and the only thing with which we can compare it would be a natural disaster. According to estimates from the United States (Federal Emergency Management Agency), only 60% of companies survive a natural disaster, and an additional 25% disappear within the first year after the disaster. Even more gloomy statistics are reported by the United States Small Business Administration who found that over 90% of companies fail within two years of being struck by a disaster. If applied to Sweden, the consequences of the pandemic in Sweden may be the collapse of hundreds of thousands of SMEs and the subsequent mass loss of both jobs and incomes. The strain on the general welfare offering will be unprecedented, as social benefits to unemployed and marginalized groups spiral, while the public income tax, the main source for welfare financing, drops.

One especially exposed and vulnerable group of small-scale business owners are those with foreign backgrounds. When it comes to accessing financial services such as loans, credits or external equity (needed to grow their businesses), they were lagging behind well before the COVID-19 outbreak. This applies in particular to foreign-born women who tend to rely more on public support or loans from family members and less on traditional bank loans, according to a report from The Swedish Agency for Economic and Regional Growth. This is at least partly to blame on the too stiff financial market regulations which the banks have to follow. Microfinance institutions in developing countries instead operate with specifically designed and adapted microfinance regulations. Just like in developing countries, this particular group of entrepreneurs typically only have limited collateral in Sweden as well, like different forms of self-owned property that can be used as collateral. They also lack a prior track record with a bank. Their new networks are also often limited and discrimination can not be ruled out. Perhaps unexpectedly, research and experience from other countries as well as indications from state-owned venture capital agency Almi suggest that the credit worthiness of these types of businesses actually is good.

A foundation in social capital and microfinance

Social capital theory, in the version originating from the American political scientist Robert Putnam in the 1990s, is conceived as the common value of not only public tangible property but also the human capital in society, building on inter personal relationships, shared norms, cooperation, trust, and reciprocity. A society with increasing segregation and inequality where large groups feel marginalized and excluded leads to weaker social capital and mistrust. In his study of the vibrant business life in the cohesive northern Italian communities, as compared to southern depressed and conflict-ridden ones, Putnam argued that it was the high presence of social capital that accounted for the success of the former.

Examples of new initiatives addressing the value of social capital in society can be found in our common efforts envisioned as part of the 17 UN SDGs. Domestic financial institutions, both banks and institutional investors, are increasingly adapting to the SDG expectations. As yet the focus has been mostly on supporting green financing where Sweden has taken a global lead. The banks have developed offerings for green credits and loans, as well as the issuance of green bonds on the capital market. The four large banks in Sweden (Nordea, Handelsbanken, Swedbank and SEB) are signatories of the United Nations Environment Program (UNEP) finance initiative, “Principles for Responsible Banking”. A number of European banks are already developing programs for domestic social impact credits, guarantee programs and loans. SEB hosts a number of microfinance funds, all targeting developing microfirms in developing countries. Swedish banks that wish to score on sustainability metrics could thus develop similar offerings for the domestic Swedish market.

New instruments, such as microfinancing and guarantee-backed loans to entrepreneurs, are potentially of high interest also to domestic institutional investors as part of their sustainability policy. For example, Swedish institutions have as part of their bond portfolio invested in Spanish and French sustainability bonds that address financing to SMEs and microfirms in depressed regions. Others have supported the World Banks’s COVID-19 programs targeting SMEs in developing countries. These and previous programs include loans to financial institutions offering microcredits. Swedish investors may be persuaded to focus to a larger extent on the socially labelled UN sustainable development goals in Sweden and not only abroad. Over the past 20 years, Swedish institutional investors have invested in 20 different socially labeled bond issues, of which only two target Sweden. Socially labeled bonds are bonds where the use of proceeds is earmarked for social or green projects.

Besides the provision of financial services to unemployed or low-income individuals who do not have access to mainstream banking services, microfinance also involves other components such as business training and insurance. Through small loans, microcredits with subsidized interest rates, and business training, the 2006 Nobel laureate Professor Muhammad Yunus and the Grameen Bank laid the foundation of the microfinance industry starting in the early 1970s. Yunus argued that the lack of financial services and the excessive capital costs for the poor led to diminished entrepreneurial opportunities. He showed that this group of individuals were both creditworthy and able to improve their lives when mobilizing and receiving credit and training.

While microfinance in a developing country context has had limited effects on business growth, microfinance does provide a form of social insurance and extra income in societies lacking a welfare system. In addition, the effects can be measured in more dimensions than creditworthiness, such as increased empowerment and self-esteem.

In a Swedish welfare context on the contrary, the use of microfinance implies changes to the welfare system, which currently builds on the assumption that individuals outside of the labor market are only temporarily unemployed. In for instance France, the NGO Adie has developed a practice to support the vulnerable traveler population with microcredits to support their microenterprises and register their informal business activities, supporting 19 000 microbusiness and creating 15 000 new jobs in 2019 alone. Here the French government and other government institutions provided vital support, including start-up subsidies and other support, in order to build the necessary strategic alliances between institutions in society such as the employment office and chamber of commerce, who with varying but overlapping social missions helped in Adie’s mission to create an arena for self-employment through microenterprises.

Sweden has had a modest history of offering microloans; so far, SEK 500 million in lending has been made available through the state-owned Almi and the privately-owned Marginalen Bank, on the back of guarantees from the EU and administered by the European Investment Fund (EIF). The general interest in these programs from other banks has been low, even though some positive signs can be seen. During the COVID-19 pandemic the so-called Företagsakuten (“The corporate emergency program”) has been established as a government-backed guarantee program for loans to Swedish corporations. However, while the scheme has some received criticism, more than 60 banks so far have chosen to join. This is an unpreceded initiative as regards domestic and government-backed guarantees, a practice previously mostly focused on export-oriented corporations or focused on international development programs.

A paradigm shift in society

With increasing migration, a rich country like Sweden has seen a rise in the number of people excluded from the traditional labor market and instead forced to live on different forms of social benefits. Inequality and segregation lead to an erosion of social capital, which in turn carries huge indirect costs. With COVID-19, everything changes. Saving jobs has never been more important and the Swedish government has launched an initial rescue plan of more than SEK 300 billion (approximately EUR 28 billion), which is likely to increase significantly. COVID-19 opens up for new initiatives that can contribute to an inclusive society with increased trust and cohesion. Social capital is on the rise again.

Engström & Oxelheim (2013) have previously introduced the possibility of using microfinance, with low interest rates, and business training, to make it easier for individuals with good ideas and dreams to become entrepreneurs or self-employed. The logic behind lower interest rates for this particular group of entrepreneurs is that the alternative cost to society is the cost of unemployment. In fact, Sweden is already an active promoter of microfinance and microenterprises internationally through for example Sida and Swedfund. Sweden can draw on the international experience to develop microfinancing also for a Swedish context. To succeed, there is a need to develop a domestic social financial infrastructure that includes the buy-in from public and private financial institutions, and civil society, that may be manifested through for instance the use of financial guarantees and social investment funds.

Yet the scale of the two existing initiatives by the state-owned lender Almi and the private bank Marginalen Bank, approximately 3 300 microloans averaging SEK 150 000, is far from sufficient to meet the needs of the Swedish microenterprises and SMEs in general and the needs of entrepreneurs with foreign background in particular. Given the higher risks of newly started businesses, loans under the current initiatives are associated with some administrative fees as well as interest rates that are often higher than the one offered to established companies. In addition, the loans have difficulties reaching the most marginalized groups. Even though the EIF demands a smaller interest rate discount for companies in the microloan program, the annual interest rate of these loans often range between 4 and 9%. This means that small businesses most often have to deal with higher capital costs than large, established companies. Lastly, the current initiative is struggling to reach 13.3% of the workforce who could work.

In other words, the new form of microfinance we are proposing is in a market segment where current actors are active to a limited extent, which is principally due to higher risks and somewhat larger difficulties in assessing the repayment capability, combined with low profitability when servicing the segment. This implies that there should be no competition between a governmental and the private alternatives.

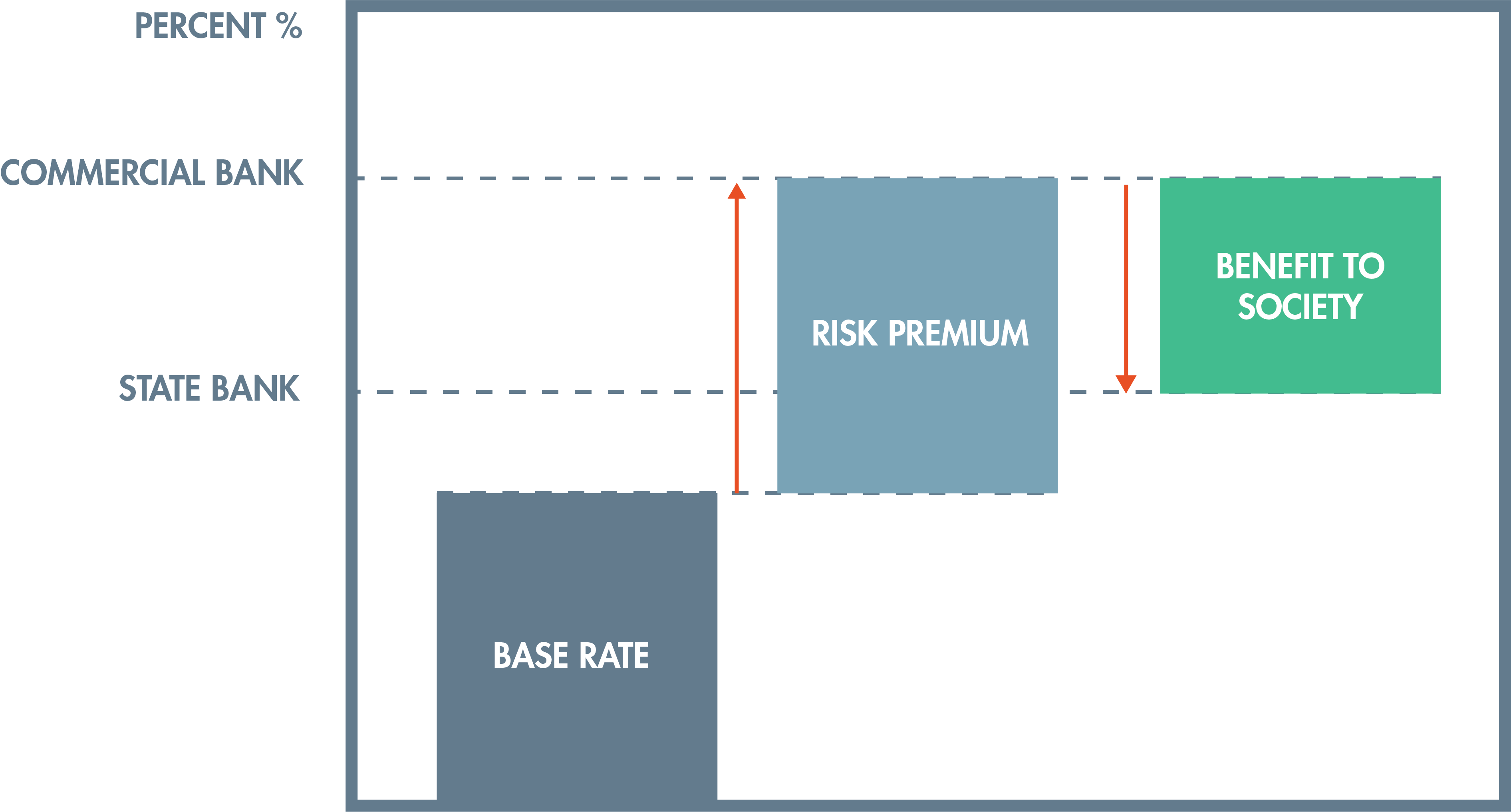

The risk and benefit assessment is fundamentally different between a private actor and a state actor. A private bank lends money to microenterprises according to its financial risk appetite, knowing that the whole portfolio of loans needs to be optimized and balanced to compensate for the fact that some of the loans will not be repaid.

For a state owned lender, on the other hand, the whole calculation looks different with other benefits that also need to be included. Unlike the private owner, such an actor enjoys all the positive social and financial effects from supporting these businesses. The successful businesses, perhaps some even creating other jobs, will move people from unemployment to employment, contributing to higher tax revenues and reduced costs to society as a result of lower unemployment and reduced social exclusion. To conclude, the risk willingness but also the benefits for a state owned lender are different to that of a privately owned bank, and thus implies different lending rates, see graph below.

There is already a structure in place in Sweden where the government offers loans with a subsidized interest rate, and that is to all university students, non-discriminary and not taking into consideration collateral or financial track record. Even those with a debt with the Swedish Enforcement Authority are able to obtain a loan. If a private bank lent money to these students, a much higher interest rate would be charged in addition to a request for collateral.

The EIF has a portfolio of programs with the aim of increasing the availability of financing to microenterprises and SMEs to support growth and increase employment rates in the EU. These programs have been widely used in the EU by private, often smaller, banks. In Sweden, however, the interest has so far been relatively low. The EIF microloan guarantee instrument addresses all microenterprises but specifically aims to targets young entrepreneurs under the age of 35 years and entrepreneurs with foreign background, and there is also a focus on gender equality. Both Almi and Marginalen Bank use the program to lower the threshold since the guarantee rate of 80% reduces the need of additional securities from the entrepreneur. Therefore, personal guarantees and collaterals could be reduced to a minimum 10-20% of the total loan amount while keeping the entrepreneur still with some risk exposure. Outside the EIF program, 100% personal guarantee is the norm.

We propose three measures to improve the current situation and truly shift the focus towards addressing large groups of currently excluded citizens. These measures combined have large potential to improve the quality of integration as well as government finances and the funding of the welfare state. In this initiative, the focus on microenterprises and SMEs is key.

-

Inclusive financing of marginalized groups: Microfinance as an initiative that specifically targets marginalized groups in society excluded from the mainstream financial system can be achieved through a state and private backed credit guarantee fund. Example of such funds already existing in Europe are the British Big Lottery Fund, Finnish Sitra, French CDC (Caisse des dépôts et consignations), the state-run investment bank Ppifance, and the cooperative bank Crédit coopératif. From a Swedish perspective, Allmänna arvsfonden [the Swedish Inheritance Fund], with a capital of SEK 10 billion, could receive a similar broadened mandate. The mandate of Almi could also be revamped, as well as the anachronistic mandate of the Nordic Investment Bank. We further propose the Swedish government maintains Företagsakuten after the COVID-19 pandemic, and to direct it towards microenterprises and SMEs, with a higher focus on guarantee schemes backing microfinance initiatives.

-

Introducing a new form of microfinance: The existing form of microloans in Sweden needs to be complemented by a completely new set of loans, governed by a separate form of microfinance regulation that allows for more favorable repayment schemes, lower administrative fees and interest rates well below commercial rates. Since the financing initiative is targeting individuals with good ideas and capabilities, but who are excluded from traditional bank financing, the risk premium on lending rates is actually negative to the state, even before taking the state guarantees into account.

-

Domestic technical assistance initiatives: Servicing the marginalized groups of society involves significant work. Civil society in addition to public, such as schools and universities, and private institutions can be mobilized to apply their resources and special competences through the provision of incentives to carry out training programs in collaboration with the financing institutions. Examples of such actors include a revamped Swedish Public Employment Office (Arbetsförmedlingen), NyföretagarCentrum, Drivhuset, Coompanion and Stiftelsen Ester. Offering independent support is crucial to improve successful entrepreneurship at all levels of society, not just among marginalized groups.

Revitalizing the Swedish welfare model post COVID-19

Prior to COVID-19, the share of the potential work force living on social benefits made up over 13%. In a Swedish welfare-state context, the marginalization of large groups from the labor market will lead to an erosion of social capital, resulting in increased levels of mistrust and alienation in society. With the COVID-19 crisis, even more individuals risk ending up in marginalization and living on social benefits.

At the same time, the crisis may be the catalyst needed to turn the development 180 degrees. We lay out the foundation for a new model for microfinance, adapted to the Swedish welfare state, including new necessary regulation and support mechanisms, such as business training and guarantee schemes. Sweden already has, through Sida and Swedfund, vast experience and technical know-how in how to run microfinance and guarantee schemes. This will also be a good opportunity for Swedish banks to live up to UNEP’s finance initiative “Principles for Responsible Banking”.

In order to revitalize the Swedish welfare model, to make the best use of society’s common funds, and to make many more individuals financially self-sufficient, we propose a new government-backed financing and support initiative. The initiative should be seen as a labor-market measure and an effort to include marginalized groups. This program will also have a positive effect on the general welfare budget as part of the costs of the mass-unemployment expected to follow the COVID-19 crisis is reduced.

References

Armendáriz, B. (2009). Microfinance for self-employment activities in the European urban areas - Contrasting Crédal in Belgium and ADIE in France. Centre Emile Bernheim, Research institute in Management Sciences.

Engström, P., & McKelvie, A. (2017). Financial literacy, role models, and micro-enterprise performance in the informal economy. International Small Business Journal, 35(7), 855-875.

Engström, P., & Oxelheim, L. (2014, July 18). Nya grepp krävs för att främja företagande. Svenska Dagbladet, 6. http://www.svd.se/nya-grepp-kravs-for-att-framja-foretagande_3750486

Nachemson-Ekwall (2019) A Swedish market for sustainability-related and socially labelled bonds. Institutional investors as drivers. SSE Working Paper Series in Business Administration, Stockholm School of Economics. No 2019:3. December. https://swoba.hhs.se/hastma/paper/hastma2019_003.1.pdf

The Authors

Pontus Engström is an affiliated researcher at the House of Innovation, Stockholm School of Economics. He is co-founder of MTI Investment AS.

Sofia Altafi has a PhD from Stockholm School of Economics. She is President and co-founder of the Ester Foundation (Stiftelsen Ester).

Sophie Nachemson-Ekwall is Research Fellow at the Centre for Research on Sustainable Markets (CRSM) at SIR, Stockholm School of Economics Institute for Research.

Gabriel Karlberg has a PhLic from Stockholm School of Economics. He is a business developer at Marginalen Bank and a serial entrepreneur.