The bleak economic future of Russia

Is the Russian economy “surprisingly resilient” to sanctions and actions of the West? The short answer is no. On the contrary, the impact on Russian growth is already very clear while the economic downturn in the EU is small. The main effects from the sanctions are yet to be realized, and the coming sanctions will be even more consequential for the Russian economy. The biggest impacts are however those in the longer run, beyond the sanctions. Mr. Putin’s actions have led to a fundamental shift in the perception of Russia as a market for doing business. The West and especially EU countries are on a track of divesting their economic ties to Russia (in particular in, but not only, energy markets) and the country is simultaneously losing significant shares of its human capital. All these effects mean that the long-term economic outlook for Russia is not just a business cycle type recession but a lasting downward shift.

Introduction

The global economic outlook at the moment seems rather bleak. According to the International Monetary Fund’s (IMF) most recent World Economic Outlook, global growth is expected to slow from above 6 percent in 2021, to 3.2 percent this year, and 2.7 percent in 2023. For the US and the Euro area the corresponding numbers are slightly above a 5 percent growth in 2021, between 2 and 3 percent in 2022, while barely reaching 1 percent in 2023. At the same time inflation is up and central banks are trying to curb this by raising interest rates.

From an EU perspective it is an open question what proportion of the lower growth is caused by the economic consequences of the Russian invasion of Ukraine. Certainly, energy prices are affected as well as issues relating to natural resources and agricultural products (though the consequences of shortages in these goods are far larger for Middle Eastern, North African and Sub-Saharan countries). But it is not the case that all of the economic problems in the EU are due to the changed economic relations with Russia.

In assessing the economic impact of Russia’s war, and in particular the impact of sanctions, it is important to focus on both expectations as well as proportions. A widespread narrative portrays Russia’s relative economic resilience (compared to the expectations of some in March/ April 2022) as the Russian economy being surprisingly unaffected, while the EU is depicted as being badly hit, especially by high energy prices. In a European context, the Swedish daily newspaper Dagens Nyheter claims that “experts are surprised over Russia’s resilience” and the Economist, a British weekly newspaper, recently portrayed recession prospects for Europe as “Russia climbs out”. We argue that such point of view is misleading. To get a more balanced image of what is unfolding it is important to think both about the expected consequences of sanctions, including how long some of them take to have an effect, but also (and maybe most important when thinking about the long run), what economic consequences are now unfolding beyond the impact of sanctions.

Sanctions against Russia

Let us start with what sanctions are in place, what types of impact these have had so far and what can be expected in the future. There are three types of sanctions currently in place. First, and most impactful in the short run, are limitations on financial transactions, especially those imposed on the Central Bank. In this category there are also the restrictions on other Russian banks disconnecting them from a key part of the global payment system, SWIFT, as well as measures targeting other assets: divestments from funds, investment withdrawals, asset freezes, and other impediments to financial flows. The main short-term aim of these actions was to reduce the Russian government’s alternatives to finance the army and their military operations. Second there are sanctions on trade in goods and services. At the moment these target particularly technology imports and energy and metals exports. These take a longer time to be felt and are potentially more costly to the sanctioning countries as well. They also contribute, in principle, to reduced resources for war. Besides affecting the government’s budget, both financial and trade sanctions disturb ordinary people’s lives as well and might create discontent and protests. A third group of sanctions are so-called sanctions of inconvenience such as limitations to air traffic, closure of air space, exclusion form sport and cultural events, restrictions of movement for both officials and tourists, and others, which aim at disconnecting the target country from the rest of the world. These are partly symbolic in nature, but can also impact popular opinion, including among the elites. However, a potential problem is that such sanctions can push opinion in either of two opposite directions: against the target regime in sympathy with the sanctioning parties; or against what is now perceived as an external enemy in a so-called rally-around-the-flag effect.

Along these dimensions the sanctions have so far had mixed effects in relation to the objectives listed above. We will return to this issue below, but in short, the sanctions on the Central Bank and the financial system, albeit powerful, fell short of causing anything like a collapse of the Russian financial system. Some of the trade restrictions, together with other global economic events, created an environment where lost trade volumes for Russia were compensated by price increases in resources and energy exports. When it comes to restrictions on imports of many high-tech components, these are certainly being felt in the Russian economy although still not fully. Public perceptions in Russia are hard to judge from the outside, especially given the problems of voiced opposition in the country, while public perceptions in sanctioning countries have mainly been favorable as people want to see that their governments are “doing something”.

What do we know about sanctions in general?

A key question when judging whether sanctions “work” is to study what a reasonable benchmark can be. As discussed in a previous FREE Policy Brief (2012), sanctions don’t enjoy a reputation of being very effective. This is true both in the research literature as well as in the public opinion. There are reasons for this that have to do with both how “effectiveness” is intended and the limits that empirical enquiries necessarily face in trying to answer the question of effectiveness. This does not mean, however, that sanctions have no effect. Another FREE Policy Brief (2022) summarizes a selection of the most credible research in this area. In short, a majority of studies find that sanctions affect the population in target countries through shortages of various kind (food, clean water, medicine and healthcare), resulting in lower life expectancy and increased infant mortality. The types of effects are comparable to the consequences of a military conflict. In the cases where it has been possible to credibly quantify the damage to GDP, estimates are in the range of 2 to 4 percent of reduced annual growth over a fairly long period (10 years on average and up to 3 years after the lifting of sanctions). One has to keep in mind that lower growth rates compound over time, so that the total loss at the end of an average period is quite substantial. As a comparison, the latest estimate of the total loss in global GDP from the Covid-19 crisis stands at “just” -3.4 percent. Other studies find similarly significant negative effects on other economic outcomes such as employment rate, international trade, public expenditure, the value of the country’s currency, and inequality. There is of course variation in the effects depending on the type of sanctions and also on the structure of the target economy. Trade sanctions tend to have a negative effect both in the short and long run, while smart sanctions (i.e. sanctions targeting specific individuals or groups) may even have positive effects on the target country’s economy in the long run.

Sanctions and the current state of the Russian economy

When it comes to the Russian economy’s performance in these dire straits, the very bleak forecasts from spring 2022 have since been partly revised upwards. Some are surprised that the collective West has not been able to deliver a “knock-out blow” to the Russian economy. In light of what we know about sanctions in general this is perhaps not very surprising. Also, one can recall that even a totally isolated Soviet economy held up for quite some time. This however does not mean that sanctions are not working. There are several explanations for this. As already mentioned, some of the restrictions imply by their very nature some time delay; large countries normally have stocks and reserves of many goods – and on top of this Mr. Putin had been preparing for a while. Also, the undecisive and delayed management of energy trade from the EU reduced the effectiveness of other measures, in particular the impact of financial restrictions. Continued trade in the most valuable resources for the Russian government together with spikes in prices (partly due to the fact that the embargo was announced several months ahead of the intended implementation) flooded the Russian state coffers. This effect was also enlarged by the domestic tax cuts on gasoline prices in many European countries in response to a higher oil price (Gars, Spiro and Wachtmeister, 2022). This is soon coming to an end, but at the moment Russia enjoys the world’s second largest current account surplus.

The phenomenal adaptability of the global economy is also playing in Russia’s favor: banned from Western markets, Russia is finding new suppliers for at least some imports. However, although they are dampening and slowing the blow at the moment, it is difficult to envision how these countries can be substitutes for Western trade partners for many years to come.

The Russian economy beyond sanctions

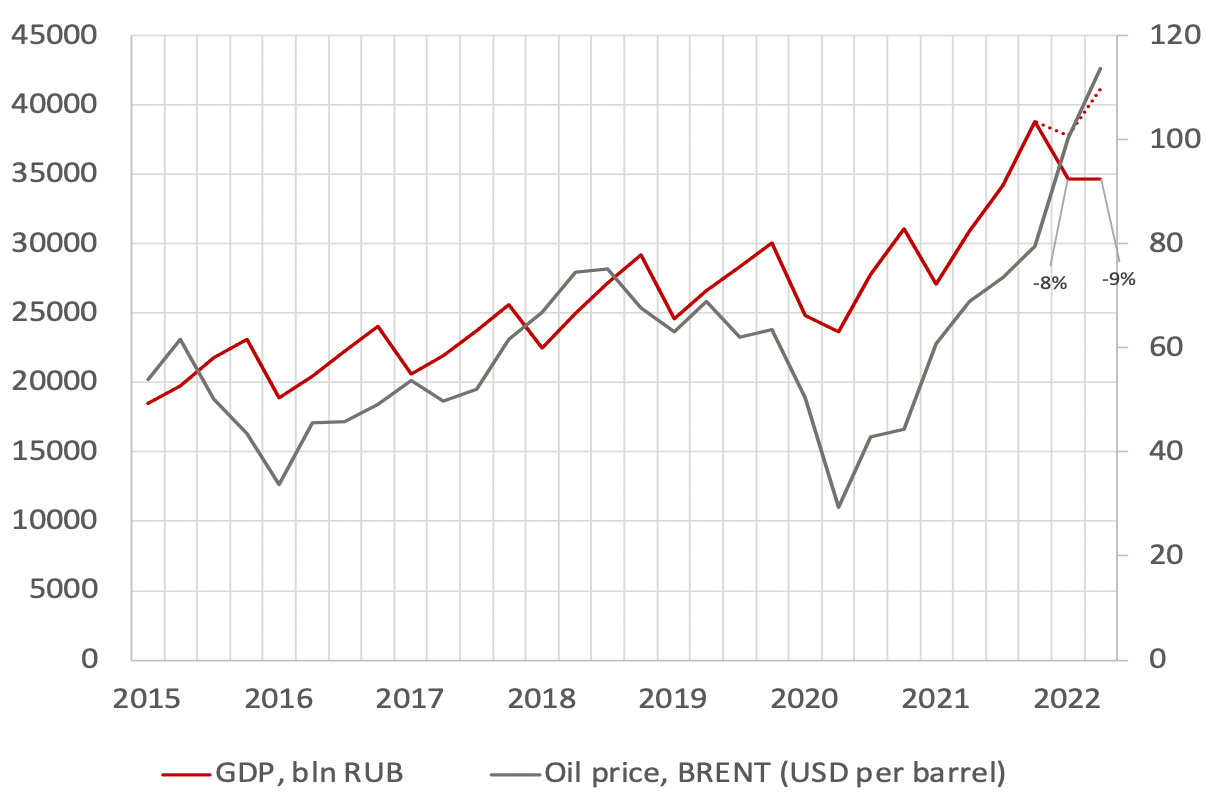

Given all of this, the impact on the Russian economy is not nearly as small as some commentators claim. Starting with GDP, an earlier FREE Policy Brief (2016) shows how surprisingly well Russia’s GDP growth can be explained by changes in international oil prices. This is true for the most recent period as well, up until the turn of the year 2021-2022 and the start of hostilities, as shown in Figure 1. Besides the clear seasonal pattern, Russian GDP (in Rubles) closely follows the BRENT oil price. This simple model, which performs very well in explaining the GDP series historically, generates a predicted development as shown by the red dotted line. Comparing this with the figures provided by the Russian Federal State Statistics Service, Rosstat, for the first two quarters of 2022 (which might in themselves be exaggeratedly positive) indicates a loss by at least 8 percent in the first and further 9 percent in the second quarter. In other words, GDP predicted by this admittedly simple model would have been 19 percent higher than what reported by Rosstat in the first half of 2022. As a comparison, Saudi Arabia – another highly oil dependent country – saw its fastest growth in a decade during the second quarter, up by almost 12 percent.

Figure 1. Russian GDP against predictions

Source: Authors’ calculations on GDP in rubles based on figures from Rosstat and the BRENT oil price series. Note that GDP is denominated in Rubles to avoid confusion due to the USD/Rubles exchange rates being volatile (given the lack of trade post invasion) and thus hard to interpret.

Other indicators point in the same direction. According to a report published by researchers at Yale University in July this year, Russian imports, on which all sectors and industries in the economy are dependent, fell by no less than ~50 percent; consumer spending and retail sales both plunged by at least ~20 percent; sales of foreign cars – an important indicator of business cycle – plummeted by 95 percent. Further, domestic production levels show no trace of the effort towards import substitution, a key ingredient in Mr. Putin’s proposed “solution” to the sanctions problem.

Longer term trends

There are many reasons to be concerned with the short run impact from sanctions on the Russian economy. Internally in Russia it matters for the public opinion, especially in parts that do not have access to reports about what goes on in the war. Economic growth has always been important for Putin’s popularity during peace time (Becker, 2019a). In Europe it matters mainly because a key objective is to make financing the war as difficult as possible, but also to ensure public support for Ukraine. A perception among Europeans that the Russian economy is doing fine despite sanctions is likely to decrease the support for these measures. However, the more important economic consequences for Russia are the long-run effects. Many large multinational firms have left and started to divest from the country. There has always been a risk premium attached to doing business in Russia, which showed up particularly in terms of reduced investment after the annexation of Crimea in 2014 (Becker, 2019b). But for a long time hopes of a gradual shift and a large market potential kept companies involved in Russia (in some time periods more, in others less). This has however ended for the foreseeable future. Many of the large companies that have left the Russian market are unlikely to return even in the medium term, regardless of what happens to sanctions. Similarly, investments into Russia have been seen as a crucial determinant of its growth and wellbeing (Becker and Olofsgård, 2017), and now this momentum is completely lost.

Energy relations have been Russia’s main leverage against the EU although warnings about this dependency have been raised for a long time. In this relationship, there has also been a hope that Russia would feel a mutual dependence and that over time it would shift its less desirable political course. With the events over the past year, this balancing act has decidedly come to an end, if not permanent, at least for many years to come. The EU will do its utmost not to rely on Russian energy in the future, and regardless of what path it chooses – LNG, more nuclear power, more electricity storage, etc. – the path forward will be to move away from Russia. Of course, there are other markets – approximately 40 percent of global GDP lies outside of the sanctioning countries – so clearly there are alternatives both for selling resources and establishing new trade relationships. However, this will in many cases take a lot of time and require very large infrastructure investments. And perhaps more important, for the most (to Russia) valuable imports in the high-tech sector it will take a very long time before other countries can replace the firms that have now pulled out.

Yet another factor that will have long-term consequences is that many of these aspects are understood by large parts of the Russian population, and those with good prospects in the West have already left or are trying to do so. It has been a long-term goal for those wanting to reform the Russian economy, at least in the past 20 years, to attract and put to fruition the high potential that have been available in terms of human capital and scientific knowledge. However, these attempts have not succeeded and the recent developments have put a permanent end to those dreams.

Conclusion

In the latest IMF forecast, countries in the Euro area will grow by 3.1 percent this year and only 0.5 percent in 2023. In January the corresponding numbers stood at 3.9 percent and 2.5 percent. This drop, caused in large part by the altered relations with Russia, is certainly non negligible, and especially painful coming on the heels of the Covid-19 crisis. However, it is an order of magnitude smaller than the “missed growth” Russia is experiencing. When judging the impact from sanctions on the Russian economy overall, the correct (and historically consistent) counterfactual displays a sizable GDP growth driven by very high energy and commodity prices. Relative to such counterfactual, the sanctions effect is already very noticeable. In the coming months, economic activity will slow down and many European household will feel the consequences. In this climate it will be important that, when assessing the situation with Russia perhaps performing better than expected, the following is kept in mind. Firstly, Russia is still doing much worse compared to the EU as well as to other oil-producing countries. Secondly, and even more important, what matters are the longer run prospects. And these are certainly even worse for the Russian economy.

References

Disclaimer: Opinions expressed in events, policy briefs, working papers and other publications are those of the authors and/or speakers; they do not necessarily reflect those of SITE, the FREE Network and its research institutes.

Photo by Miha Creative, Shutterstock.com