Does the Russian stock market care about Navalny?

For many significant Navalny news stories, the stock market experienced large negative returns that are not explained by the regular factors that move the market. Although the causality and permanency of these negative excess returns in the stock market are difficult to pin down completely, a first look at the numbers suggests that the short-run drops in the stock market on the days with most significant news regarding Navalny translates into several billion dollars in lost market value on the Russian stock market. In other words, for people that care about their stock market investments and the health of the Russian economy more generally, it makes a lot of sense to care about the health of Navalny.

Introduction

Alexei Navalny has become the leading political opponent to the current regime in Russia. His visibility (and possibly support) has been growing as he has endured poisoning, recovery in hospital, and court rulings that have imposed a harsh prison term. At the same time, Navalny and his team have posted new material online to make his case that both the president and other Russian leaders are seriously corrupt.

The question addressed in this brief is whether the news regarding Navalny affected the Russian stock market. The reasons for such a response may vary between different investors but could include a fear of international sanctions against Russia; an aversion to keeping investments in a country that put a nerve agent in the underwear of a leading opposition leader; or that news of a national security service poisoning one of its own citizens could trigger domestic protests that create instability.

This brief only investigates if Navalny-related news or events are taken into account at the macro level in the stock market and if so, how important the news seem to be relative to other news as drivers of the stock market index. However, there is a long list of related questions that are subjects for upcoming briefs that include differential effects across sectors and companies as well as identifying what dimensions of the news stories investors responded to.

Navalny in the News

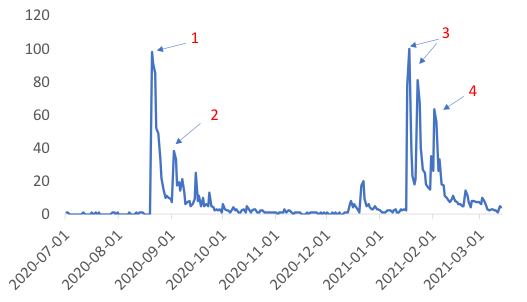

Since August 2020, news regarding Alexei Navalny’s health and his role as the most important opposition leader in Russia have featured prominently in media around the world. There are different ways to analyze the significance of Navalny in the news and here the readily available measure provided by Google trends will be used. Figure 1 shows a global search on the keyword “Navalny” over the period July 1, 2020 to March 13, 2021 relative to total searches, where the maximum level in the period is normalized to 100 and other values are scaled to this. While the numbers on the graph are just relative measures, not telling much about the actual popularity, or market relevance of searches, the spikes in Figure 1 have very clear connections to major news stories as will be detailed below.

Figure 1. Google trends on Navalny

Source: Google trends, global search on Navalny on 2021-03-18

Four episodes stand out in Figure 1 and are marked by red numbers:

1 (August 20-25, 2020) is associated with Navalny falling ill on the flight from Tomsk to Moscow which led to an emergency landing in Omsk and then going to Germany for specialist treatment where it was stated that he had been poisoned.

2 (September 2-3, 2020) is when the German government said that the poison Navalny was exposed to was Novichok, which was also confirmed by laboratories in Sweden and France.

3 (January 17-25, 2021) is an extended period covering the arrest of Navalny as he returned to Russia on January 17; the publication of the YouTube video on “Putin’s palace”; and the street protests that followed.

4 (January 31-February 5) is a period covering a new weekend of public protests and then on February 2, Navalny being sentenced to prison for not complying with parole rules when he was in a coma in Germany. At the tail end of this period, Navalny’s chief of staff announced that street protests will be suspended due to thousands of arrests and police beatings.

Russian Stock Market Reactions

Using stock markets to investigate the value of political news is not new; for example, Fisman (2001) looks at how news regarding Suharto’s health differentially impacted firms that were connected to Suharto versus those that were not. On a topic more closely related to this brief, Enikolopov, Petrova, and Sonin (2018), show that Navalny’s blog posts on corruption negatively affect share prices for the exposed state-controlled companies. Looking at the overall stock market index rather than individual shares in Russia, Becker (2019) analyzes stock market reactions to Russia invading Crimea.

To get a stock market valuation effect of Navalny news that is as clean as possible, we need to filter out other factors that are known to be important drivers of the stock market. In the case of Russia’s dollar denominated stock market index RTS (short for Russia Trading System), we know from Becker (2019) that it is sensitive to movements in global stock markets and international oil prices. The former factor is in line with other stock markets around the world and the oil dependence of the Russian economy makes oil prices a natural second factor (see Becker, 2016).

Figure 2 shows how the RTS index moves with the global markets (proxied by S&P 500 index) and (Brent) oil prices in this period. The correlations of returns are around 0.4 between the RTS and both S&P500 and oil prices respectively. This figure is also the answer to the obvious argument that the stock market was doing very well in the time period of Navalny in the news, so he could not be a major concern to investors. As we will show below, this argument goes away when the effects of the exogenous factors are removed.

To filter out these exogenous factors, we follow the approach in Becker (2019) and regress daily returns on the RTS on daily returns of the exogenous variables. We then compute the residuals from the estimation to arrive at the excess returns that are utilized in the subsequent analysis. For more details on this, see Becker (2020). Since the estimated model provides the foundation for the subsequent analysis, it is important to note that all of the coefficients are statistically significant, and that results are robust to changes in the estimation period and exclusion of lagged values of the exogenous variables.

Figure 2. RTS and exogenous factors

Source: Data on RTS from the Moscow Exchange (MOEX), S&P500 from Nasdaq, and Brent oil prices from the US energy information administration.

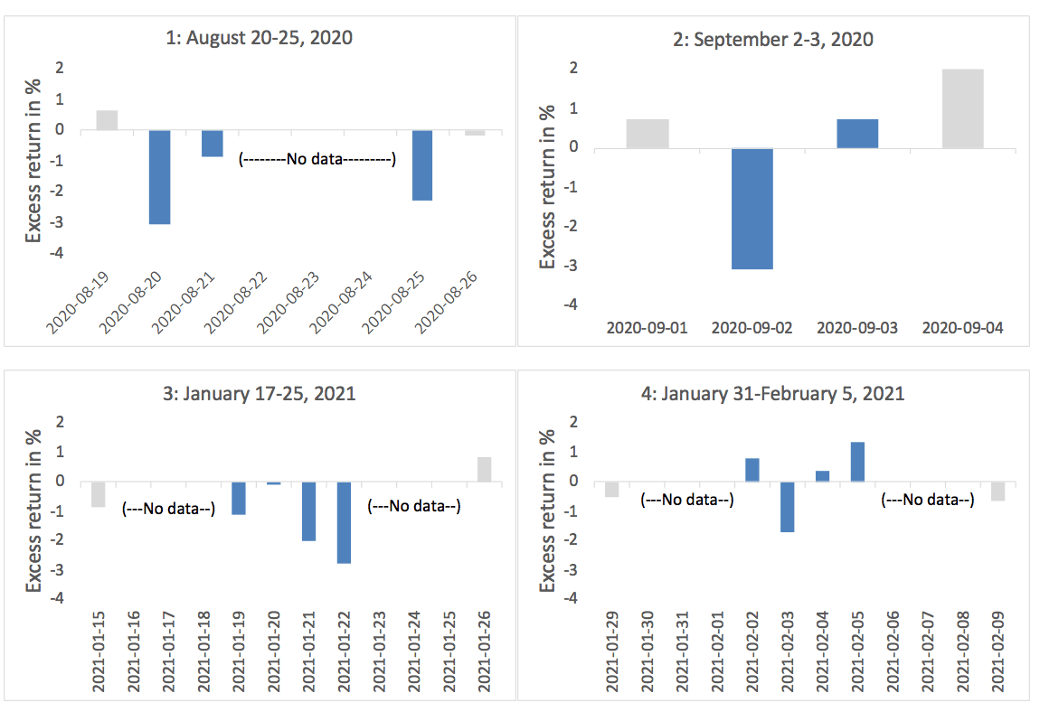

With a time-series of excess returns for the Russian stock market, we can look at the stock market reactions to the four Navalny episodes identified in Figure 1. These periods cover some days for which we cannot compute excess returns since there are days when there is no trading, but all dates in the period are shown in Figure 3 to provide a full account of what stock market data we have for the events. In addition to excess returns during the events that are shown in blue, the day before and the day after the events are shown in light grey. In the first three episodes, the cumulative returns during the events windows were minus 6.2, minus 2.4, minus 6.0 percent, while in the fourth event window it was plus 0.8 (although in this period, the day after Navalny was sentenced to jail, the excess return was minus 1.7).

The correlations between news and excess returns in this brief are based on daily data. Since many things can happen during a day, the analysis is not as precise as in the paper by Enikolopov, Petrova, and Sonin (2018), where the authors claim that causality is proven by the minute by minute data. Although we have to be more modest in claiming that we have identified a causal relationship going from Navalny news to negative stock market returns, the daily data used here provides enough evidence to claim that there is a strong association pointing in this direction. If we take all four events and translate the cumulative excess returns in percent (which is 14) into dollars by using the market capitalization on the RTS at the time of the events (on average around 200 billion dollars), this amounts to a combined loss in market value of over 27 billion dollars.

Figure 3. Excess returns and Navalny news

Source: Excess returns from author’s calculations based on data from the Moscow Exchange (MOEX), Nasdaq, and the US energy information administration. The chart indicates days for which we cannot compute excess returns since not all days are trading days.

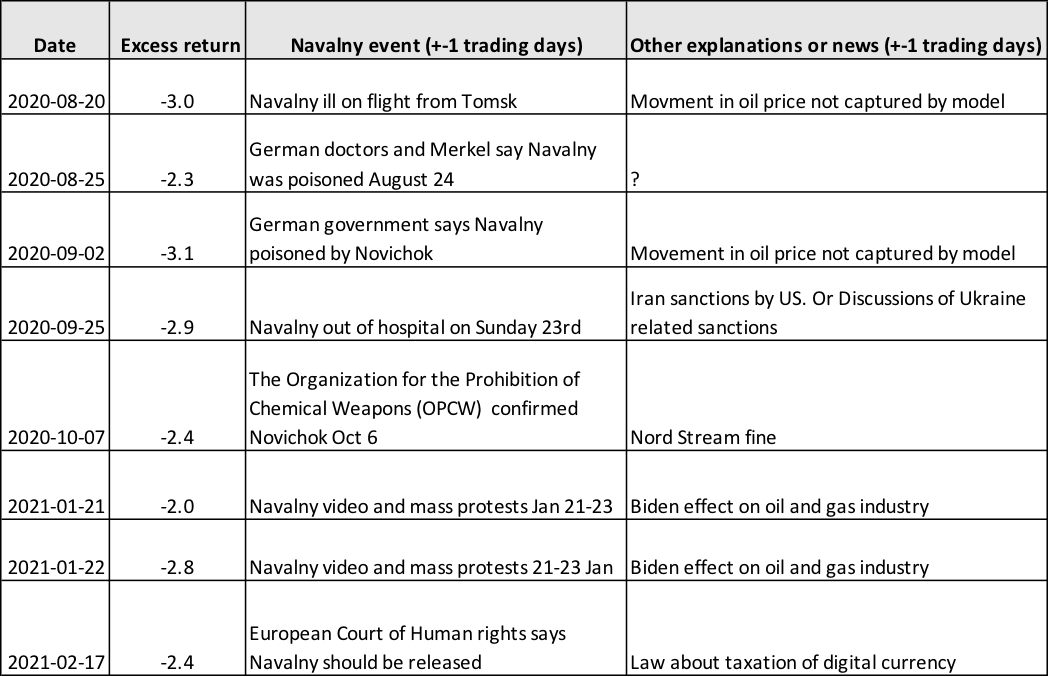

We may think that excess returns of this magnitude are common and that what we pick up for the four Navalny episodes are regular events in the market. To investigate this and other potential factors that have been important to explain excess returns in this time period, Table 1 provides a list of all the days when the excess return in the market was minus 2 percent or worse. Between August 2020 and mid-March 2021, there were eight such days. The table also shows what could be an associated Navalny event on or close to those dates as well as other competing factors or news that could explain the large negative returns on these days.

Out of 8 days with strong negative returns, the first three days are very clearly associated with major news regarding the poisoning of Navalny. The fourth day is close to Navalny’s release from the hospital but also when there are discussions about U.S. views on Iran and Ukraine. Two of the days are in the time period of the protests following Navalny’s video on “Putin’s palace” and two more days are related to important international institutions speaking out regarding first the poisoning with Novichok and then about the prison term of Navalny.

Although we would need a more fine-grained look at market data to make a final judgment on the most important drivers of the excess returns of a specific day, the fact that every single day with large negative excess returns is on or close to a Navalny news story is again pointing in the direction of a stock market that reacts to news about Navalny. Furthermore, the most significant drops with less competing news are associated with events that have a direct connection to Navalny’s health and how his life was put in danger. In the list of competing news are Nord Stream, Biden affecting the oil and gas industry, and a law regarding the taxation of digital currencies. They are likely to be of at least some relevance for stock market valuations and could account for certain days or shares of poor performance of the RTS, but it is hard to ignore the general impression of Navalny being important for the stock market in this period.

Table 1. Days with RTS excess returns of minus 2% or worse (August 1, 2020 to March 12, 2021)

Source: Excess returns from author’s calculations based on data from the Moscow Exchange (MOEX), Nasdaq, and the US energy information administration. News comes from internet searches on Navalny and relevant dates.

Conclusions

Although it is difficult to prove causality and rule out all competing explanations, this investigation has shown a strong association between major news regarding Navalny and very poor performance of the Russian stock market. Every day since August 2020 that had excess returns of minus 2 percent or worse is more or less closely associated with significant news on Navalny. More than that, almost all days with significant Navalny news during this period, – as captured by high search intensity of Navalny on Google, – are associated with a poorly performing stock market. In particular, this holds for the day of his poisoning and the following days with comments by international doctors, politicians, and institutions regarding the use of Novichok to this end.

It could be noted that a 1 percent decline in the RTS equates to a loss in monetary terms of around 2 billion USD in this time period since the market capitalization of the RTS index was on average around 200 billion USD. The combined decline in the events shown in Figure 3 is 14 percent and for the days listed in Table 1, it is 21 percent, i.e., corresponding to market losses of somewhere between 28 and 42 billion USD. Even if only a fraction of this would be directly associated with news on Navalny, it adds up to very significant sums that some investors have lost. One may argue that the losses are only temporary and recovered within a short time period (which would still need to be proven), but for the investors that sold assets on those particular days, this is of little comfort. At a minimum, events like these contribute to increased volatility in the market that in turn has a negative effect on capital flows, investments, and ultimately economic growth (Becker, 2019 and 2020). For anyone caring about the health of their own investments or the Russian economy, it makes sense to care about the health of Navalny.

References

- Becker, Torbjörn, 2016. “Russia and Oil — Out of Control”, FREE policy brief.

- Becker, Torbjörn, 2019. “Russia’s Real Cost of Crimean Uncertainty”, FREE policy brief, June 10.

- Becker, Torbjörn, 2020. “Russia’s macroeconomy—a closer look at growth, investment, and uncertainty”, Ch 2 in Putin’s Russia: Economy, Defence And Foreign Policy, ed. Steven Rosefielde, Scientific Press: Singapore.

- Enikolopov, Ruben, Maria Petrova, and Konstantin Sonin, 2018, “Social Media and Corruption”, American Economic Journals: Applied Economics, 10(1): 150-174.

- Fisman, Raymond, 2001, “Estimating the Value of Political Connections.” American Economic Review, 91 (4): 1095-1102.

- Google trends data.

- Moscow Exchange (MOEX), RTS index data.

- Nasdaq, S&P 500 data.

- U.S. Energy Information Administration, 2021, data on Brent oil prices.

Disclaimer: Opinions expressed in policy briefs and other publications are those of the authors; they do not necessarily reflect those of SITE, the FREE Network and its research institutes.