Exploring the impact from the Russian gas squeeze on the EU’s greenhouse gas reduction efforts

Throughout 2022, the reduction in Russian gas imports to the EU and the resilience of European energy markets have been subject of significant public discourse and policy-making. Of particular concern has been the EU’s ability to maintain its environmental goals, as substitution from Russian pipeline gas to liquified natural gas and other fuels such as coal, could result in increased emissions. This brief aims to reevaluate the consequences from the loss of Russian gas and the EU’s response to it on greenhouse gas emissions in the region. Our analysis suggests that the energy crisis did not result in a rise in emissions in 2022. While some of the factors that contributed to this outcome – such as a mild winter – may have been coincidental, the adjustments caused by the 2022 gas squeeze are likely to support rather than jeopardize the EU’s green transition.

Energy markets in Europe experienced a tumultuous 2022, with the Russian squeeze on natural gas exported to the region bringing a major shock to its energy supply. Much attention has been devoted to the effects of the succeeding spiking and highly fluctuating energy prices on households’ budget and on the production sector, with numerous policy initiatives aimed at mitigating these effects (see, e.g., Reuters or Sgaravatti et al., 2021). Another widely discussed concern has revolved the consequences of the gas crisis – such as switching to coal – on the EU’s climate policy objectives (see e.g. Bloomberg or Financial Times). In this brief we analyze and discuss to what extent this concern turned out to be valid, now that 2022 has come to an end.

We consider greenhouse gas (GHG) emissions stemming from the main strategies that allowed the EU to weather the gas crisis throughout 2022 – namely the substitution from Russian gas to other energy sources. These strategies include increased imports of liquified natural gas (LNG), a lower gas demand, and an increased reliance on coal, oil, and other energy sources. We also discuss the implications of the crisis for climate mitigation in the EU and try to draw lessons for the future.

Substitution to LNG and pipeline gas from other suppliers

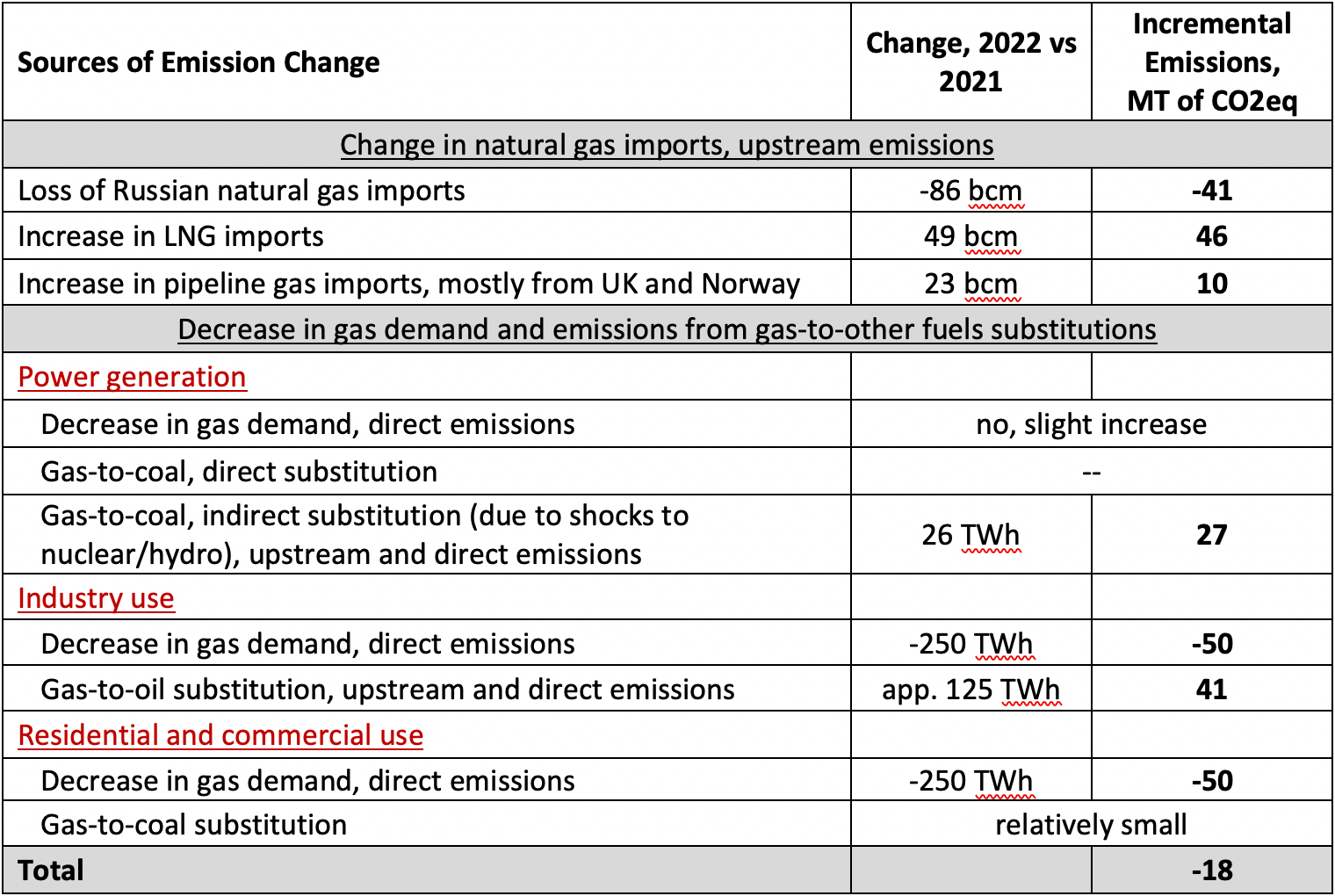

Prior to 2022, Russian natural gas largely reached Europe by pipeline (92.4 percent in 2021 according to Eurostat). More than half of these pipeline imports, 86 billion cubic meters (bcm), were lost during the 2022 Russian gas supply squeeze, predominantly through the shut-down of both the Yamal and the Nordstream pipelines. 57 percent of this “missing” supply was met through an increase in LNG imports from several countries, the largest contributor being the U.S. Another 27 percent of the “missing Russian gas” was substituted by an increase in pipeline gas imports from other suppliers, with the UK (20 percent) and Norway (7 percent) taking the lead. A substantial part of the replaced gas was stored, rather than combusted. With this in mind, here we concentrate on the upstream emissions associated with this change – i.e., emissions that occurred during the extraction, processing, and transportation. The change in the combustion emissions is postponed to the next section.

There is an ongoing debate in the literature on whether the greenhouse gas pollution intensity of LNG is higher or lower than that of gas delivered through pipelines – prior to final use. In comparison to pipeline gas, LNG is associated with emissions resulting from energy-intensive liquefaction and regassification processes in upstream operations as well as with fuel combustion from transportation on ocean tankers. For both LNG and pipeline gas it is also crucial to consider fugitive methane emissions, as methane has up to 87 times greater global warming potential than carbon dioxide in the first 20 years after emission, and up to 36 times greater in the first 100 years. One source of methane emissions is leaks from the natural gas industry (both “intentional” and accidental) since methane is the primary component of natural gas. Both LNG and pipeline gas infrastructure are subject to such leaks, and the size and frequency of these leaks during transportation varies greatly depending on the technologies used, age of infrastructure, etc. Further, the risk of these leaks may also be different depending on the technology of gas extraction.

Currently there is limited knowledge about the size of greenhouse gas emissions, including methane emissions resulting from leaks, from specific gas projects. Until recently, most estimates were based partially on self-reported data and partially on “emission factors” data. Modern and more reliable methods, for instance satellite-based measures for methane emissions, suggest that the resulting figures are greatly underestimated (see, e.g., Stern, 2022; IEA; ESA) but the coverage of these new estimates is currently limited.

As a result, there is considerable disagreement in the literature on the emissions arising from Russian pipeline gas imports vs. LNG imports to the EU. For example, Rystad (2022) argues that the average LNG imports to Europe have a CO2 emission intensity that is more than 2.5 times higher than that from pipeline gas from Russia (although they do not explicitly state whether these figures include fugitive methane emissions). On the contrary, Roman-White et al. (2019) suggest that the life-cycle GHG emission intensity of EU LNG imports (from New Orleans) is lower than EU gas imports from Russia (via the Yamal pipeline).

For the purposes of this exercise, we choose to rely on middle-ground estimates by DBI and Sphera, which assess GHG emission intensity along different Russian gas import routes (DBI, 2016) and across different LNG suppliers to the EU (Thinkstep – Sphera, 2020). This allows us to account for substantial heterogeneity across routes.

We also account for the change in upstream emissions associated with the switch from imports of pipeline Russian gas to pipeline gas imports from Norway and the UK. For this, we approximate the GHG emission intensity of the new flows using the estimate suggested by Thinkstep – Sphera (2017).

The results of our assessment are presented in the top three rows of Table 1. They suggest that a substitution from Russian gas imports to LNG imports and pipeline imports from other sources resulted in an increase in upstream GHG emissions by approximately 14 million tons (Mt) of CO2eq. Details on calculations and assumptions are found in the online Appendix.

Table 1. Change in EU GHG emissions resulting from Russian gas squeeze.

Source: Authors’ own calculations based on DBI (2016), McWilliams et al. (2023), Sphera (2017; 2020), and IEA (2022). See the online Appendix for more details on assumptions, calculations, and sources. Note: Billion cubic meters (bcm) and terawatt-hours (TWh).

The decline in gas demand and the switch to other fuels

A decrease in gas use in the EU constituted another response to the Russian gas squeeze. Gas demand in the EU is estimated to have declined by 10 percent (50 bcm or 500 TWh) in 2022 with respect to 2021 (IEA, 2022). Part of this decline was facilitated by switching from gas to other polluting fuels, such as oil and coal. The extent to which switching occurred however differed across the three main uses of gas; power generation, industrial production, and residential and commercial use. Below we discuss them separately.

Power generation

At the onset of the 2022 energy crisis, a prevalent expectation was that there would be significant gas-to-coal switching in power generation. However, gas demand for power generation, which accounts for 31.4 percent of the gas demand from EU countries (European Council), increased by only 0.8 percent in 2022 (EMBER, 2022, p.29), implying that there was no direct substitution from gas-fired to coal-fired generation.

One of the reasons to why there was no major switching to coal in spite of the increase in gas prices is that CO2 emissions are priced in the Emissions Trading System (ETS) program, and the average carbon price has been growing recently, reaching an average of around €80/ton in 2022. Given that coal has a higher emission intensity than gas, the carbon price increases the relative cost of coal versus gas for power generators.

Instead, the decline in demand came from industry, residential and commercial use, which together account for nearly 57 percent of the EU’s gas demand (European Council).

Industry use

For the industry, IEA calculations (2022) suggest a demand drop of 25 bcm, which would correspond to approximately 50 Mt CO2eq. However, half of the industrial gas reduction came from gas to oil switching. Based on our estimates, this switch implies an additional 41 Mt CO2eq emissions, considering both upstream emissions and emissions from use in furnaces (assuming this to be the prevalent use of the oil that substituted gas, see McWilliams et al., 2023). The remaining half of the industrial demand decline resulted from energy-efficiency improvements, lower output, and import of gas-intensive inputs where possible (ibid.). These changes are either neutral in terms of life-cycle emission impact (import increases) or emission-reducing (efficiency improvements and lower output).

Residential and commercial use

Residential and commercial use represented the remaining part of the 500 TWh gas demand decline. In this case, lower gas demand is unlikely to imply massive fuel switching to other fossil fuels, simply because of the lack of short-term alternatives. For example, European households use gas mostly for space heating and cooking, and albeit both higher use of coal for home-heating (BBC) and a surge in installations of heat pumps (Bruegel, 2023 and EMBER, 2023) have been reported, the net change in emissions resulting from these two opposite developments is likely relatively minor as compared to other considered sizeable changes.

The rise of coal

As observed, there was no direct switch from gas to coal in European power generation. However, coal generation in the EU did increase by 6 percent in 2023 (IEA, 2022), to help close the gap in electricity supply created by the temporary shut-down of nuclear plants in France and the reduced performance of hydro. In our calculations we assume that in a counterfactual world with no Russian gas squeeze, gas-fired electricity would have covered most of the gap that was instead covered by coal. Therefore, we estimate that, as an indirect result of the Russian gas squeeze in 2022, CO2eq emissions increased by 27 Mt, specifically because of the ramp-up in coal generation (see the second section in Table 1).

Gas shortage and the EU’s climate objectives

In recent years, the EU has made substantial progress in climate change mitigation. Despite widely expressed concerns, it achieved its 2020 targets – reducing emission by 20 percent by 2020, from the 1990 level. However, its current target of a 55 percent net GHG emission reduction by 2030, requires average yearly cuts of 134 Mt CO2eq, from the 2021 level. This is an ambitious target: while the emission cut between 2018 and 2019 exceeded this level, the average yearly cut between 2018 and 2021 however fell short (Eurostat).

The question is if the Russian gas squeeze can significantly undermine the EU’s ability to achieve these climate goals?

First, based on our assessment above, the changes prompted by the Russian squeeze – namely a move from pipeline-gas to LNG, a decline in gas demand and an increase in coal and oil use – made 2022 emissions decline by 18 Mt CO2eq. This suggests that the energy shock prompted overall emission-reducing adjustments in the short run. One important question that arises from this is therefore how permanent these adjustments are.

The increased reliance on LNG (and other gas suppliers) is likely to be permanent as a return to imports from Russia is hardly imaginable and as the 2022 surge in LNG imports entailed significant investments and contractual obligations. According to our estimates, overall, this shift is going to cause a relatively modest increase in yearly CO2eq emissions, approximately 10 percent of the needed emission reduction outlined above. Moreover, this is accounting for emissions throughout the EU’s entire supply chain – which is increasingly advocated for, but not currently applied in the typical emission accounting. It is, of course, important to make sure that ongoing LNG investments do not result in “carbon lock-ins”, postponing the green transition.

The decline in gas demand is a welcome development for climate mitigation if it is permanent. Part of the decline, from improved energy efficiency or installation of heat pumps, is indeed permanent. However, European households also responded temporarily (to warmer than usual winter and high gas prices (for instance by reducing their thermostats). Their behavior in the near future will therefore depend on the development of both these variables.

Overall, our assessment is that the Russian gas squeeze did force some adjustments in demand that might translate into a permanent decline in greenhouse gas emissions.

The question however remains of how the shortage of gas can be met in a scenario with higher gas demand due to, for instance, colder winters. In terms of climate objectives, it is of paramount importance that coal-powered generation does not increase (which would happen if, for instance, the price of gas continues to raise due to shortages). In this sense some lessons can be learned from the response to the shortage in electricity supply following the exceptional under-performance of nuclear and hydro in 2022. Wind and solar, which provide the lowest-cost source of new electricity production, in combination with declines in electricity demand, were able to cover 5/6 of the 2022 shortage created by the nuclear and hydro shock (EMBER, 2023), thus relegating coal to a residual contribution. We expect this pattern to emerge also in the future in the presence of other crises. However, we also caution that the lower production of electricity was at least partially caused by the dramatic heatwaves and droughts experienced throughout the summer in Europe. These events are likely to happen more often in the face of climate change. European policy-makers should therefore carefully assess the capacity of the EU energy system to address potentially multiple and frequent shocks with minimal to no-reliance on coal, in a scenario where also reliance on gas needs to be in constant decline given the Russian gas squeeze and unreliability.

Finally, the dramatic circumstances of 2022 led the EU to adopt the REPowerEU plan, which outlines financial and legal measures to, among other things, speed up the development of renewable energy projects and induce energy-saving behavior.

The outlined observations lead us to conclude that the Russian gas squeeze is ultimately unlikely to sizably reduce the chances of the EU reaching its climate goals, suggesting that the 2022 concerns in this regard were somewhat exaggerated. Nonetheless, learning from the costly lessons of the 2022 energy crisis is crucial for efficient policy making in the future.

Authors

References

Disclaimer: Opinions expressed in events, policy briefs, working papers and other publications are those of the authors and/or speakers; they do not necessarily reflect those of SITE, the FREE Network and its research institutes.

Photo by vchal, Shutterstock.com