Debt accumulation and the value chain

In this article, Tomas Hjelström and Torbjörn Sällström discuss potential effects of debt accumulation. Comparing industrial and service firms, they highlight risks that occur when several companies in a value chain accumulate massive debts. If companies survive short term by accumulating debt instead of issuing new equity, the long-term prospects for the larger eco-system might be very negative.

Tomas Hjelström and Torbjörn Sällström

Debt Accumulation and the Effects on the Value Chain?

The COVID-19 pandemic has clearly put severe financial pressure on many companies around the world. National and international organizations and governments have tried to alleviate the situation with a multitude of efforts, for instance permitting short-term layoffs, introducing rent reliefs and providing capital injections to the banking system. Despite these coordinated efforts, many companies have already filed for bankruptcy. However, business mortality per se will not be discussed here. Instead, focus on what will happen to the firms who survive this pandemic will be addressed. We will thus consider important concepts of liquidity and solvency and discuss the difficult trade-off between short-term survival and long-term financial strength. There is a real concern that company balance sheets (statements of financial position) will be severely weakened because of the pandemic. Rebuilding the financial strength of companies using only internally generated funds will probably take several years, in some cases maybe as long as ten years if external capital injections by owners are not provided. We argue that this financial fragility will have long-term consequences on supply chains in virtually all industries. Companies emerging relatively unharmed from the crisis will probably need to provide financial support to weak firms in their supply chain to secure uninterrupted flows of inputs to their own production processes. Furthermore, we analyse the financial impact of higher corporate debt in companies because of economic crises in general and the COVID-19 crisis in particular. We discuss the long-term effects of this unwanted debt position for the future competitive conditions of the individual companies and the survival of their supply chains.

Ways to handle the current liquidity shortage

Many companies around the globe have suffered dramatically during the first half of 2020. Demand for their products and services has fallen between 10 percent to 100 percent, except in a few select industries like food and medical supplies where demand has increased. This sudden reduction in demand puts dramatic strain on the financial situation of firms that find themselves having difficulty meeting their short-term obligations due to a lack of liquid funds. These obligations are both operational and financial in kind. Operating obligations include tax payments, supplier invoices and customer reimbursements as well as fixed costs such as salaries and rents. On top of that, most firms also have short-term financial obligations like interest payments on outstanding liabilities and amortization of existing debt. All these obligations must be served with liquid funds of different kind. Effectively, what sources of liquidity are available to these firm? Two important internal sources of funds are: 1) current cash holdings, including short-term liquid investments; and 2) working capital assets that can be quickly converted to cash without severe drops in value, for instance, by collecting outstanding receivables or decreasing inventory levels. These internal sources are not unlimited, however, and at some point in time the situation will require external financing. In that case, only three alternatives remain: 1) borrowing; 2) selling off fixed assets; and/or 3) issue new equity.

When it comes to borrowing, governments and central banks have taken several measures to encourage bank lending to firms with short-term liquidity needs. Loan financing to solve liquidity demands seems to be the preferred alternative from the public point of view. Contrasting this view, however, some large companies like the airline SAS have argued that the solution to the funding problem cannot be to add massive amounts of new debt, especially to an already debt-burdened firm. The second alternative, selling of fixed assets, is most likely the least accepted solution among firms since it has serious long-term effects on the production capacity and post-crisis operating abilities. The third alternative, new equity, is probably the only one available to companies without fixed assets to provide as collateral or with substantial amounts of intangible assets on the balance sheet. Here we typically find companies in the service industry and in research driven sectors. But because of lower transparency in small and medium-sized companies, it is hard to evaluate these effects empirically. We will probably not see the full effect of the crisis until the release of the 2020 financial statements, starting in the latter half of 2020 for the companies with fiscal year ending in mid-2020. However, we have learned from previous crises that corporate debt levels tend to increase rapidly, and we will discuss these effects and focus on the practical implications of higher debt levels for firms and industries below.

An illustration of liquidity shortage and financial strength during a severe crisis

To illustrate the financial effects of a sudden and severe fall in demand, we will study two different stylized cases, one goods-producing industrial firm and one firm based in the service sector. We will calculate the impact of a large drop in sales on income statements and balance sheets, focusing on expected changes in a few key financial ratios commonly used to measure liquidity and financial strength. The examples are chosen to illustrate how these two very different types of companies may be affected by the current crisis from a financial perspective, and how the change in financial strength in turn may impact the operations of the firms and their respective intra-industry relationships. The illustrations are based on drops in sales of different magnitudes, depending on the industry, and will also consider how various expenses and working capital items will react when demand falls.

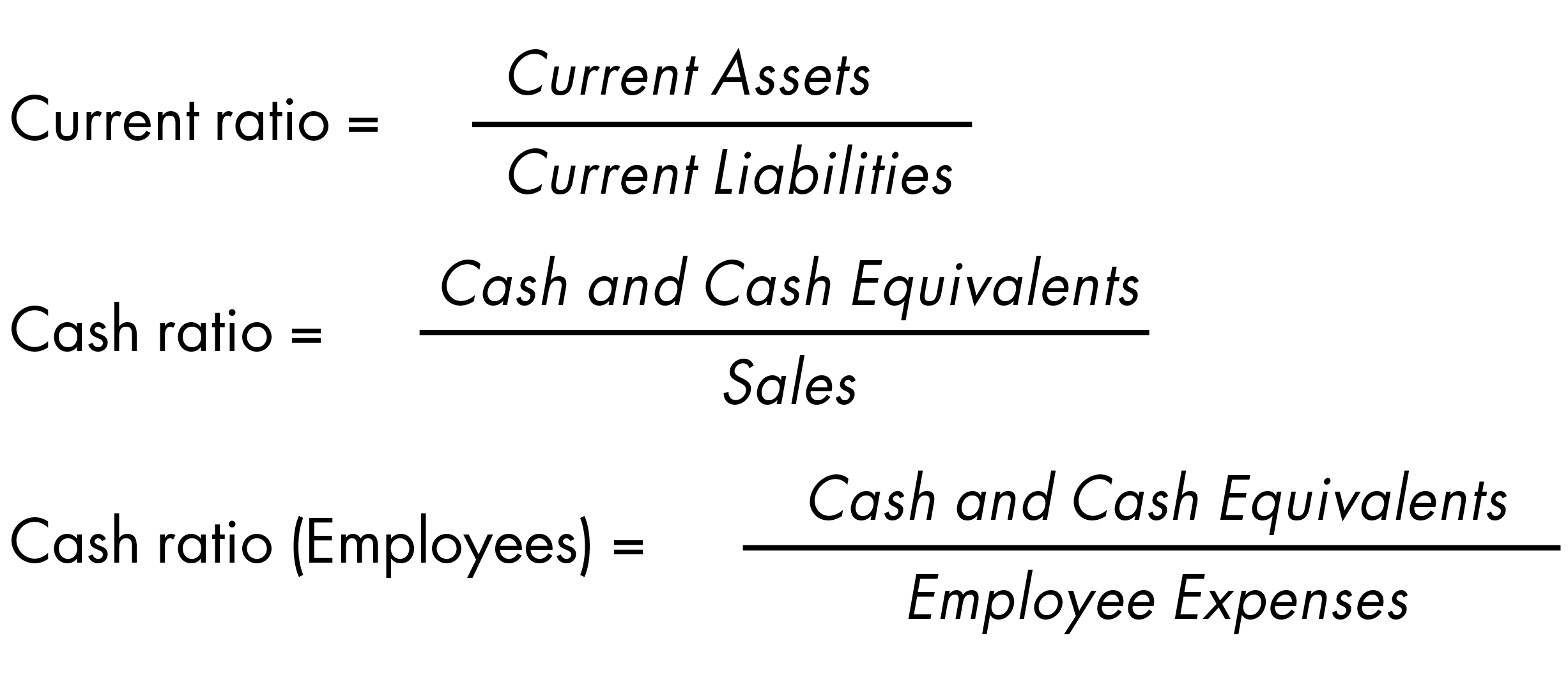

Before we move to the illustrations, we define the measures of liquidity and financial strength we will use in the scenarios. We use three different key ratios to measure the liquidity of companies. These are:

These measures capture the ability of a firm to meet its short-term payments. By short-term we typically refer to payments within a year, but we acknowledge that one year is a very long period in a deep crisis. However, the above measures are indeed more short-term than it seems since current liabilities are normally paid within one or two months, and the denominator in the two cash ratios are taken from the income statement which is gradually built up over time.

We use three different key ratios to measure the solvency of companies. These are:

These measures capture the financial strength of companies. Equity-to-assets is the traditional measure of financial strength in Sweden. The debt-to-equity measure is more common in international settings and is especially useful in integrated analyses of combined sets of key ratios. The net debt-to-equity is widely used in finance textbooks and classic finance theory. Credit rating institutes and banks also tend to use this measure extensively, since it is argued that it measures better the “real” indebtedness. However, the question of which financial assets we should deduct from interest-bearing liabilities in calculating the ratio is case-dependent and hence somewhat difficult to generalize. We would argue that many financial assets listed on the balance sheet, like cash and cash equivalents, are needed in day-to-day operations. It is often only in pure liquidation cases that the net debt position is relevant. Stated differently, the debt-to-equity is probably at least as relevant as the net debt-to-equity in measuring the level of financial strength and financial risk exposure of the company.

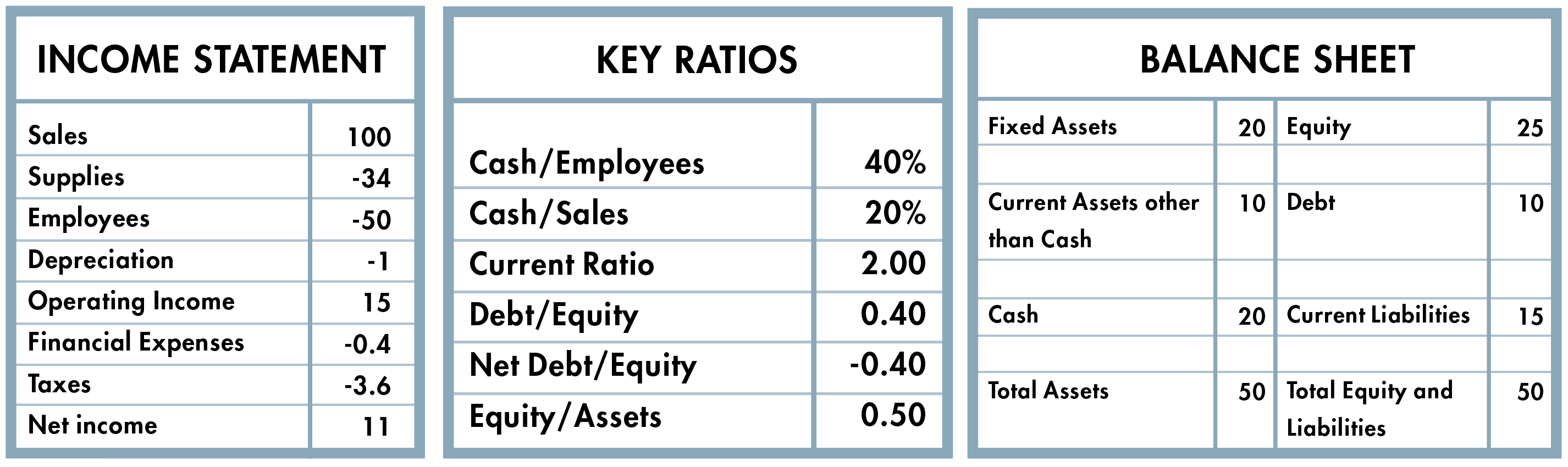

Case study 1: The industrial firm

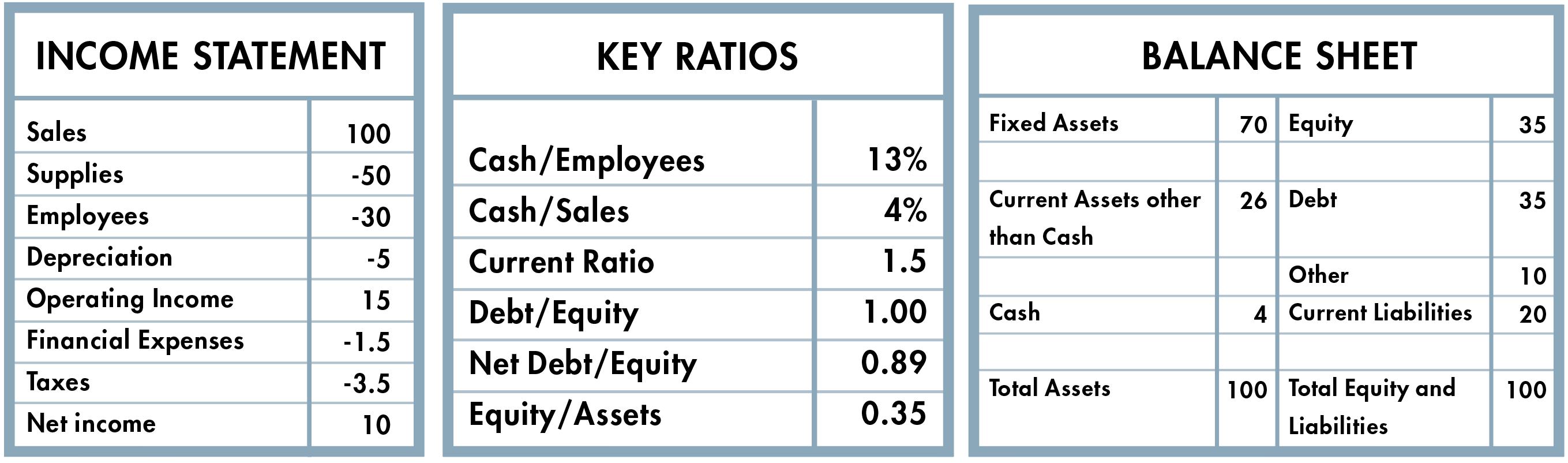

Our first illustration is an industrial firm with high profitability before the crisis. The return on equity is about 30 % which of course is a very high number. The operating margin is 15 %. Total assets correspond to one year of sales. The financial position is strong with a debt-to-equity of 1.00 and an equity-to-assets ratio of 35 %. The liquidity measures also indicate a strong financial position.

The scenario for the industrial firms is based on the following premises. All investments are postponed during the crisis, meaning that fixed assets are only affected by depreciation. Depreciation is unchanged from the income statement above. Furthermore, we assume no impairments. Current assets (primarily inventory and receivables) decrease at the same rate as sales. However, part of that decrease has an income statement effect due to uncollectible receivables and inventory write-downs. Cash is assumed to have a minimum level of 2 in order to continue operations, i.e. a reduction by 50 %. Current liabilities follow the average pattern of supplies and employee expenses, since they involve payables, withheld personal taxes, social security and other related items. Other liabilities, which include items like provisions, are reduced by 30 %. No dividends are paid to shareholders, and debt is seen as a residual to cover the liquidity needs.

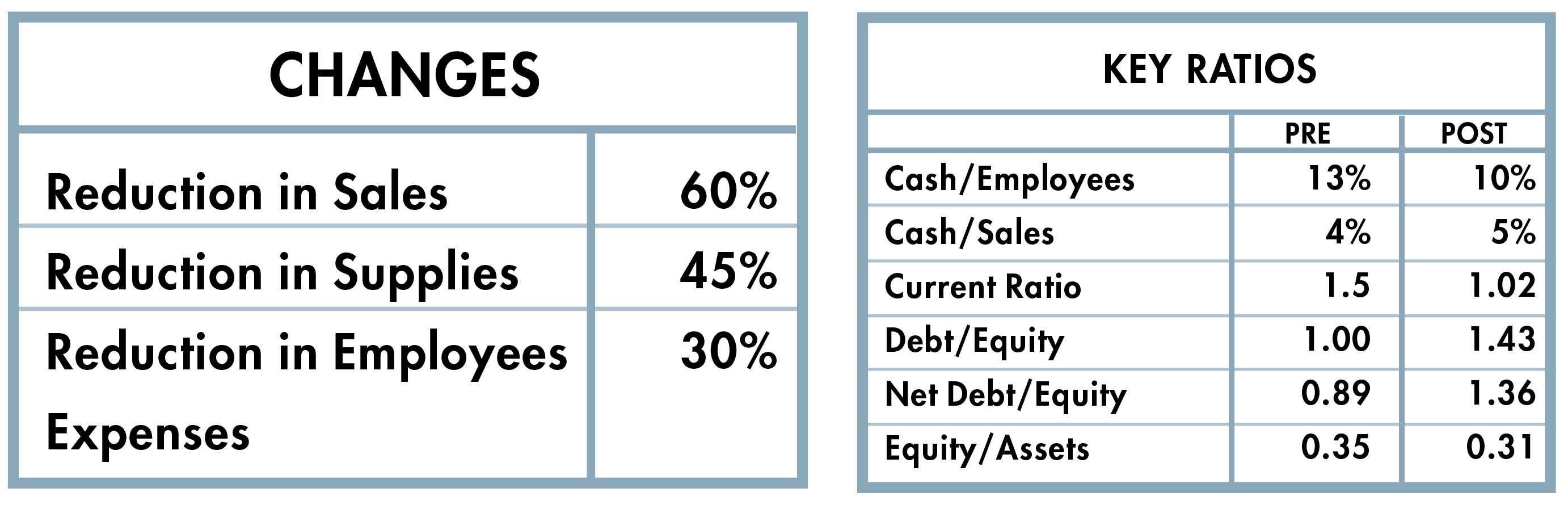

In this scenario, we study the effects of a decrease in sales of 60 %, with supplies decreasing by 45 % and employee expenses with 30 %. Below we see the calculated consequences of these changes on financial key ratios.

We see that the liquidity ratios have been kept at a comparatively good level. Cash and cash equivalents have been forced to stay positive by assumption, with a certain level of cash needed to guarantee a level that is compatible with a going concern scenario. The measures of financial strength deteriorate dramatically, however. The smaller impact on the equity-to-assets measure compared to debt-to-equity ratio is due to the simultaneous decrease in assets. The decrease in working capital liabilities is smaller than the simultaneous fall in working capital assets, which in turn keeps the debt at a lower level than would otherwise have been the case. Moreover, the company goes from being highly profitable to making losses, reducing its equity as a result.

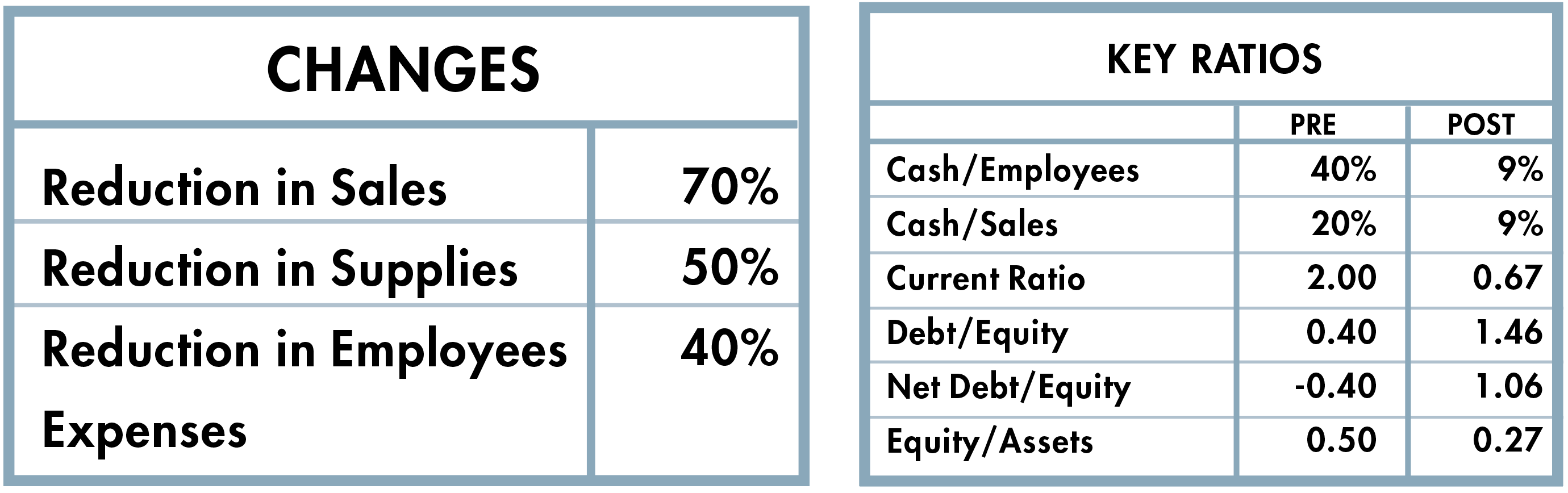

Case illustration 2: The service sector company (with some fixed assets)

Our second illustration is a service company which is also initially very profitable, with an even better position than the industrial firm on all ratios. Since this is a firm in the service sector, the balance sheet is comparatively smaller in relation to sales than for the industrial firm, about half the size, but it still contains some fixed assets. These kinds of companies therefore have some debt capacity compared to a completely service-based company such as a pure consultancy firm. The company has some initial debt, with an equity-to-assets ratio of 50 % and a debt-to-equity ratio of 0.4. The pre-crisis profitability is even higher than in the industrial company, with a return on equity of more than 40 %.

The scenario for the service firm is in all relevant aspects the same as for the industrial firm. Due to the relatively large income statement in relation to the balance sheet and the higher proportion of fixed costs, the effect on equity due to a sales decline is much more severe for the service firm than the industrial firm.

In this case, we have assumed a fall in sales of 70 %, a decrease in supplies of 50 % and a reduction in employee expenses of 40 %. We see the outcome on financial ratios below.

The effects are much more severe for the service firm than for the industrial firm we studied above. The service firm will survive, but all measures have deteriorated dramatically, and we see particularly dramatic increases in the debt-based measures of financial strength. The debt-to-equity is up to 1.46, from an original level of 0.40. Of course, one could argue that it may not be likely that credit institutions will grant loans on this scale to these kinds of firms, but we could study a less severe market situation where the firm has a higher probability of actually getting new loans. The fundamental effects on the firm from having to raise large amounts of new debt in order to survive with a fundamentally strong business, given the pre-crisis conditions, is still worth analysing.

What will happen after the crisis?

So far, we have assumed that the crisis is likely to have a strong negative impact on the financial position of all firms being hit by demand shocks. We now want to highlight three broad categories of effects relevant for the post-crisis situation. The first relates to cash flow management, the second concerns the time it will take for firms to return to the preferred “optimal” financial position through internally generated funds, and the third has to do with financial distress and its impact on company behaviour. The three categories are related, but it is important to distinguish the case of financial distress from the first two categories, which are relevant whether the firm is in financial distress or not. By financial distress, we mean that there are some likely economic scenarios in which the firm cannot meet either its interest payments or its amortizations on debt and in some instances, fails to meet both.

Let us start with the first situation, a non-financial distress scenario. Having an unusually large amount of debt on the balance sheet after the crisis puts a much higher demand on the company to generate a steady flow of cash. The debt must be serviced with both higher interest payments and increased amortization payments to revert to the preferred financial position with less debt. If the company cannot get new equity capital from its owners, the cash flow must be generated internally from the operations of the company. There are only two ways to do this. Either the company increases its margins, without losing sales, or it reduces its net working capital by reducing receivables and inventory and increasing payables. Formulated differently, it is likely that surviving companies with a weaker financial position are forced to raise sales prices, lower purchase prices, extend credit days from suppliers and shorten credit days to customers, combined with a potentially lower service level due to less inventory. These strategic measures will of course have a direct impact on all players in the industry’s value chain, including customers, suppliers, and competitors. The other players may have to provide the financially constrained companies with conditions that support the actions needed. The question is of course whether these other players have incentives to support the whole value chain. This question can only be answered by understanding the inter-dependencies and relationships between the companies and whether alternative supply sources and customers are easily available. A thorough analysis of these factors goes beyond the scope of this article. However, preparing for a competitive situation that goes beyond ordinary business negotiations is likely to be a good strategy for many companies in most industries.

Regarding the second category, the time it takes to recover from a substantial shock to the financial strength of a firm should not be underestimated. The problem involves several difficult trade-offs, such as dividend payments to shareholders versus a quick financial recovery through reinvested earnings. It is all too easy to destroy a good financial position, but it may take a very long time to recover it. Depending on the future growth of the firm, different aspects come into play. With strong growth, the level of debt may be acceptable in the long run but an extraordinary increase in equity may nevertheless be required to finance the growth. Such an increase in equity can only be realized through two sources, new issues of shares or reinvested profits. Given that shareholders probably want regular dividend payments, the burden becomes even bigger. This can be seen in the equation below, where the growth in equity is explained using the clean-surplus relation:

This relationship can be restated in terms of percentage growth rates, focusing on return on equity (ROE), dividend pay-out ratios and new equity issues as a percentage of opening equity as in the equation below:

For instance, if we need to grow equity by 40 % in order to restore the debt-to-equity relationship after the crisis to normal levels while also paying out 50 % of net income in dividends, it will take four years to get there given a 20 % ROE per year in the post-crisis period. Even in normal times, these are very challenging conditions for any firm. The time it will take to recover should therefore not be underestimated unless substantial capital contributions from owners are considered.

The third aspect mentioned above concerns financial distress. If companies experience financial distress at some point in time after the crisis due to increased indebtedness, another set of difficult conditions may enter the picture. One of those is the risk of underinvestment. Underinvestment is a situation where companies are unable to invest in value-creating opportunities due to a lack of investable funds or difficulties in raising funds from external parties, whether from credit institutions or owners. From a value chain perspective, this could, for example, mean that a subcontractor will find itself unable to make all necessary technological investments to keep up with the needs of a large customer. The solution to the problem then becomes funds from the customer to secure the deliveries. This is a risky position for all parties. Second, customer, suppliers and employees might find it unattractive to deal with a company that is on the verge of financial distress. The necessity of higher prices and better credit terms discussed previously might be very hard to achieve if the company has entered a situation of financial distress. A weak negotiation position is the outcome.

Conclusion

In this article, we have discussed short-term implications and long-term effects on financial positions of companies after a crisis such as the COVID-19 pandemic. We may summarize the findings in the following way:

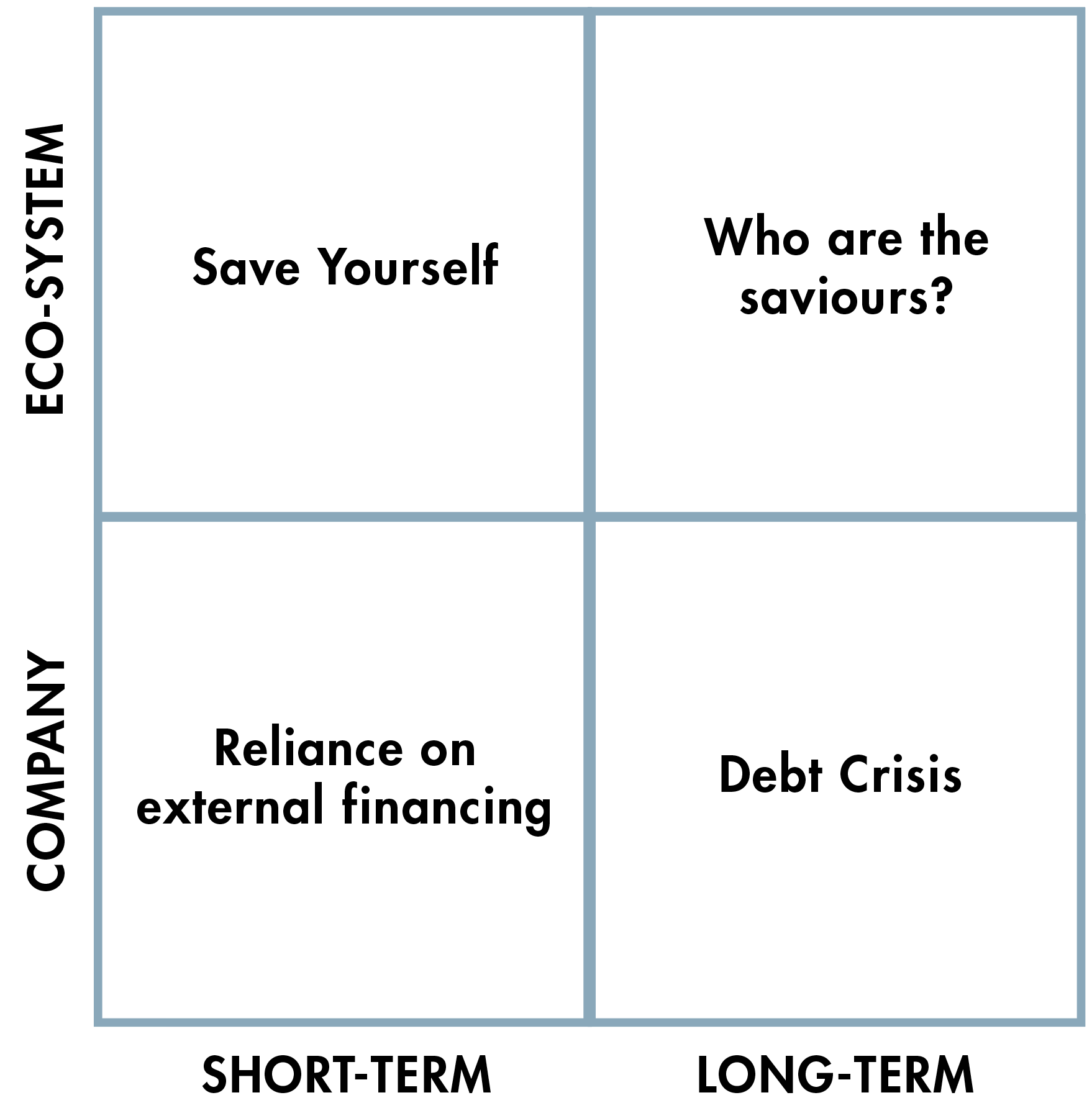

The figure shows the time-perspective on the x-axis and the level of impact on the y-axis (company level versus whole industry eco-system). The analysis and conclusions assume that companies will survive the crisis and continue operations after the crisis has passed. The short-term impact on the company is a matter of simply surviving and managing the liquidity needs. This happens during the crisis, and there is a substantial need for external financing to cope with the situation. When it comes to the industry eco-system and value chain in the short-term, we foresee that the actions taken are mainly directed towards saving the individual companies rather than the industry eco-system. This is a very natural response.

What happens after the crisis in the long-term is an illustration of the difficult times ahead. If the individual companies have relied on debt financing during the crisis, due to an inability or lack of willingness to raise equity capital, there is a risk of a severe and prolonged debt crisis. The financial strength, measured as equity-to-assets or debt-to-equity, is likely to have decreased dramatically. This puts high financial pressures on the companies in the life-after-COVID-19. From an industry eco-system perspective in the long run, one of the main questions is the development of the relationships between companies. We have framed this issue as a question of who the saviours will be, i.e. which companies will have to take a lead in financing and structuring the industry post-COVID-19. The companies that have suffered the least, most likely the champions of the systems, may be the ones who must support other necessary players in the system. We strongly urge management teams and owners to be prepared to look beyond their own companies’ short-term interests and consider the health and survival of the entire eco-system in the long run. Of course, not everyone can be saved, and mitigating actions to save the supply chain will be expensive, but the alternative of building completely new supply chains and secure new long-term relationships is also very costly indeed.

Our final thought is that we all need to prepare for the post-COVID-19 situation, because “it ain´t over ‘til it’s over” and much cooperation and preparation is needed for what is to come after the health part of the crisis is over. Stand ready!

The authors

Tomas Hjelström is Assistant Professor at the Department of Accounting at Stockholm School of Economics. He is a Program Director at SSE Executive Education.

Torbjörn Sällström holds an Ek. Lic. Degree in Finance from Stockholm School of Economics. He is a Program Director at SSE Executive Education.