The EU gas purchasing mechanism: A game-changer or a storm in a teacup?

Marking a milestone in the tumultuous journey towards a unified energy policy, the European Union (EU) member states have initiated joint procurement of a portion of their gas consumption. This coordinated effort has been facilitated through a gas purchasing mechanism, the AggregateEU, as of May 2023. In this policy brief we discuss the challenges this mechanism faces, given its design characteristics and the altered dynamics of the gas market following the energy crisis.

The necessity for a coordinated approach to energy security within the EU has been recognized at least since 2009, when its legal base was explicitly introduced in Article 194 of the Treaty of Lisbon. However, the de facto implementation of the solidarity principle has been lagging for many years. In response to the 2022 surge in gas prices, the EU has at last taken the solidarity approach to common energy security seriously. One of the most prominent steps is the creation of the AggregateEU mechanism, launched at the end of 2022. This mechanism aggregates the demand of registered buyers from different member states and matches it with competitive bids from external gas suppliers. It aims at improving and diversifying the EU gas supply, avoiding unnecessary buyer competition within the EU and building up the buyer power of EU member states. Furthermore, the mechanism is meant to reduce uncertainty and mitigate price volatility by providing information about accessible energy supplies. The mechanism covers both pipeline natural gas and Liquified Natural Gas (LNG) and organizes tenders every two months. While EU member states are required to submit demand bids for 15 percent of their 90 percent storage targets for the upcoming 2023-24 season through the mechanism, there is no obligation to sign any contracts based on the resulting match (more details can be found here and here).

The first three rounds of tendering via the mechanism, which took place May-October 2023, matched approximately 34 billion cubic meters of natural gas, exceeding the anticipated initial volumes. This outcome is currently perceived as a great achievement, enabling more vulnerable countries to benefit from coordinated purchases and resulting in increased bargaining power. Driven by this success, the European Commission (EC) has considered making demand aggregation via the mechanism a permanent feature of the EU’s gas market – and even extending it to hydrogen. However, while these agreed trades are a positive development, they may not reflect the mechanism’s overall success. Demand submission obligations may increase the number of demand calls which could project into more matches, but as they are not binding the subsequent agreements may not necessarily result in finalized contracts or lower prices.

In this brief, we argue that the mechanism’s benefits remain uncertain, primarily due to the current state of the EU’s gas market and the design flaws arising from efforts to address disparities in energy security among member states. These considerations call for a direct impact assessment, which however remains impossible due to the EC’s inability (or even reluctancy?) to collect and disclose the contracted outcomes resulting from the mechanism matches. This is especially problematic in light of the EC’s intentions to extend the mechanism’s coverage.

Limited mechanism benefits under new market trends

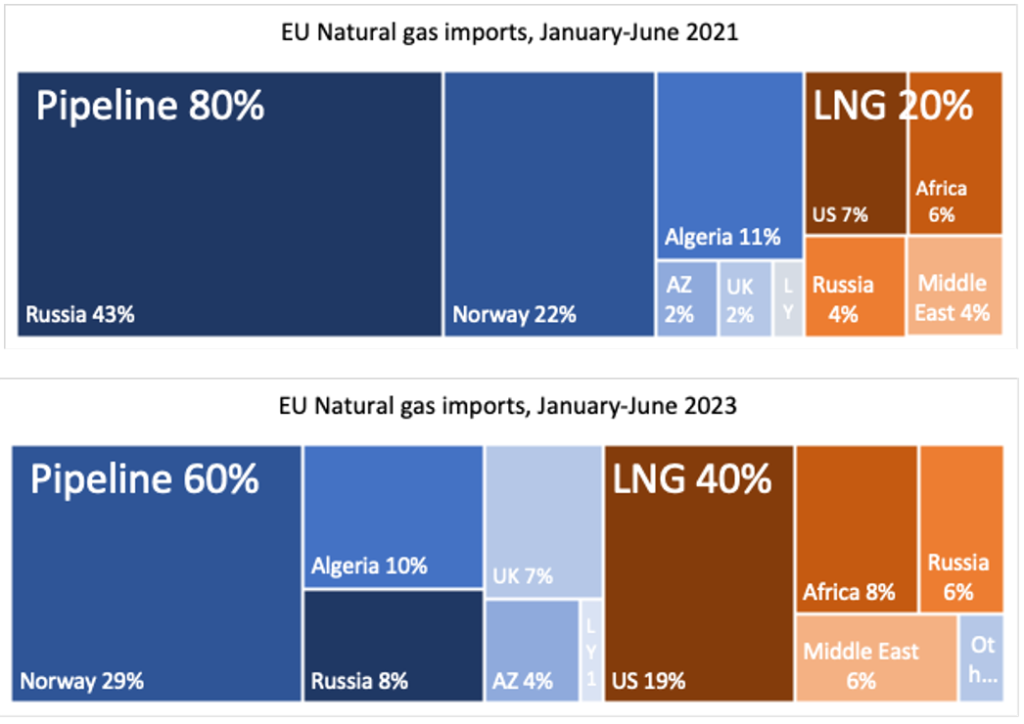

Over the past two years, the EU has undertaken drastic efforts to address the energy security concerns within its gas market caused by the radical reduction in Russia’s natural gas exports to Europe. The EU has managed to sizably improve the diversification of its gas imports (see Figure 1), fill its storage facilities, and lower its gas demand (see McWilliams, Sgaravatti, and Zachmann (2021) and McWilliams and Zachmann (2023)).

Figure 1. Composition of EU natural gas imports

Source: Authors’ calculations based on McWilliams, Sgaravatti and Zachmann (2021).

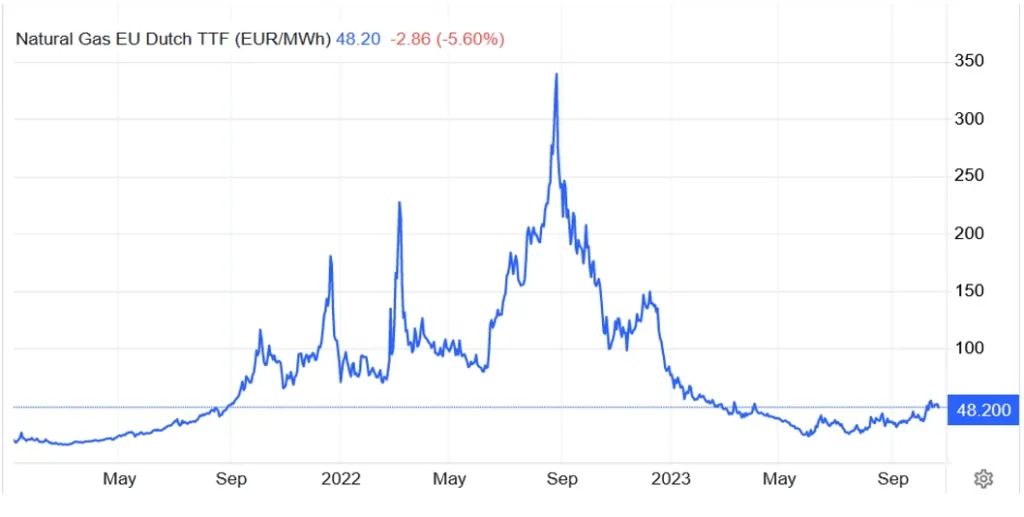

As a result, a certain balance of supply and demand has been achieved, and the gas prices in the EU market have fallen to pre-war price levels (though they are still somewhat higher than their earlier long-term trend), as depicted in Figure 2. The ease of market tensions in 2023 has led many to argue that market forces are sufficient to resolve potential problems in the EU gas market and that mechanism costs would not be justified (see, e.g., Eurogas or International Association of Oil and Gas Producers opinions).

However, in the coming years the EU gas market is expected to be relatively tight due to capacity constraints both in the LNG market and for pipeline gas producers (as noted by, e.g., Bloomberg and IEA). This tightness makes the market highly sensitive to shocks, and a twofold increase in exposure to LNG – with its global liquidity – only adds to the problem. A good illustration of this concern is the recent market reaction to the Israel-Palestine war: the fear of supply disruptions lead to a whopping 55 percent increase in the European gas tariff TTF in the second week of October and to an EC initiative to prolong the emergency gas price cap, initially introduced in February 2023. This despite the EU’s gas storage nearing 98 percent of capacity and relatively low current prices.

Such a “seller market” situation implies that buyers’ ability to exercise buyer power and negotiate down prices may be highly limited when needed the most. Specifically, buyer power would be most effective when buyers have a credible outside option, e.g., the ability to claim that their gas demand needs can be facilitated elsewhere. The tighter the market, the more difficult it would be to find such volumes elsewhere, further limiting buyers’ ability to negotiate down prices. To put it differently: current market conditions may undermine the original purpose of the mechanism.

The current “shock-sensitivity” of the gas market may also give rise to additional concerns regarding the mechanism’s mere purpose – demand aggregation for vulnerable buyers. One of the by-products of demand aggregation is that (pooled) buyers are more likely to face correlated risks, e.g., by purchasing gas from the same producer. If markets are highly shock-sensitive – as they currently seem to be – such aggregation may further increase market volatility, implying that vulnerable buyers would be affected the most.

Figure 2. Natural gas prices in the EU, January 2021-October 2023 (prices in EUR).

Source: tradingeconimics.com

Mechanism design: Constraints vs. Efficiency

Some design elements of the purchasing mechanism may also challenge the mechanism’s ability to deliver an efficient outcome. First, quantity and price under the matching process are not binding, and buyers and sellers are expected to continue negotiations individually after the matching. This feature was introduced due to the concern that it would be challenging to offer a “one size fits all” binding contract to incorporate all participants of the pooled demand. This, as argued by Le Coq and Paltseva (2012; 2022), was one of the reasons for the previous failure to implement a mutual insurance and solidarity mechanism across the EU. However, the non-binding matching outcome will likely give rise to re-negotiations, price increases, and failure to exercise consolidated “buyer power”.

Moreover, a company can act on behalf of small or financially constrained buyers, purchase gas for them, and become an “Agent-on-behalf” and “Central Buyer”. In the process, companies will inevitably exchange sensitive information. This may limit competition and increase the market power of the “Central Buyer” company. In addition, firms may choose not to participate in the mechanism for at least two reasons. First, they may fear the threat of revealing valuable private information. Second, demand aggregation may discourage market participants with stronger buyer positions from participating, as being pooled with weaker participants would undermine their bargaining power. Both these cases would create a so-called adverse selection effect, where the more performant market participants would choose to avoid the joint purchasing mechanism. As a result, the joint buyer power may be strongly undermined, and the price-suppressing effect seems uncertain. This may explain why some firms, like several large German firms, have opted to sign long-term contracts with gas suppliers directly rather than via the mechanism

Several of these concerns arise not from the mechanism design per se but rather in combination with the inherent asymmetries between EU buyers, including variations in gas demand, risk exposure, etc. To put it differently: it is well justified that a “one size fits all” approach would fail in ensuring broad (and voluntary) mechanism participation; however, the choice of a more flexible solution, as implemented by the AggregateEU mechanism, creates commitment issues and adverse selection, and may undermine an effective use of buyer power.

Impact assessment: Necessary but currently impossible

The new EU gas purchasing system is a significant step towards creating a unified energy policy. However, the design of such a procurement auction raises concerns about its contribution, especially under the new gas market dynamics. The current low gas prices make the immediate cost-benefit tradeoff of the mechanism nonobvious. More importantly, the tightness of the EU gas market in the next few years makes the “seller” power unlikely to be counteracted by the EU’s buyer power. Further, the absence of legal commitment between matched participants, and increased market volatility can lead to repeated ex-post renegotiations. These elements undermine the mechanism’s role and raise doubts about its benefits. Some of the mechanism’s inherent features, such as incentives for abuse of market power, also contribute to potential efficiency loss.

Hence, while the motivation behind this tool is clear, the implementation and potential design flaws may undermine the gains. It is therefore particularly important to understand whether the mechanism is effectively meeting its objectives, especially given the recent initiative to make it a permanent feature of the EU gas market and a key solution for the European Hydrogen Bank in the future. These considerations make a strong call for an impact assessment. An unbiased measure of AggregateEU’s impact would be necessary to assess the benefits of the mechanism (and to weigh them against the bureaucratic implementation costs). Currently, however, the EC has chosen not to collect, let alone disclose, the contractual outcomes resulting from matches. In a recent interview, Matthew Baldwin, deputy director-general at the EC’s energy directorate, said, “The reality is we’ve had relatively little feedback so far because companies are not required to give that to us in terms of the deals”. One may argue that many of the potential deficiencies of the mechanism design – e.g., non-binding matching and adverse selection – are justified by asymmetries across participants and other inherent market features. However, the absence of (appropriately desensitized) data about actual outcomes resulting from mechanism matches is more difficult to justify. The lack of data prevents us from evaluating the AggregateEU’s performance and raises additional concerns about its efficiency. Thus, gathering relevant information and conducting a comprehensive impact assessment based on sensible criteria are essential prerequisites for the future use, and expansion of the AggregateEU mechanism.

References

Disclaimer: Opinions expressed in events, policy briefs, working papers and other publications are those of the authors and/or speakers; they do not necessarily reflect those of SITE, the FREE Network and its research institutes.

Photo: Anton Zubchevskyi, Shutterstock