What does the gas crisis reveal about European energy security?

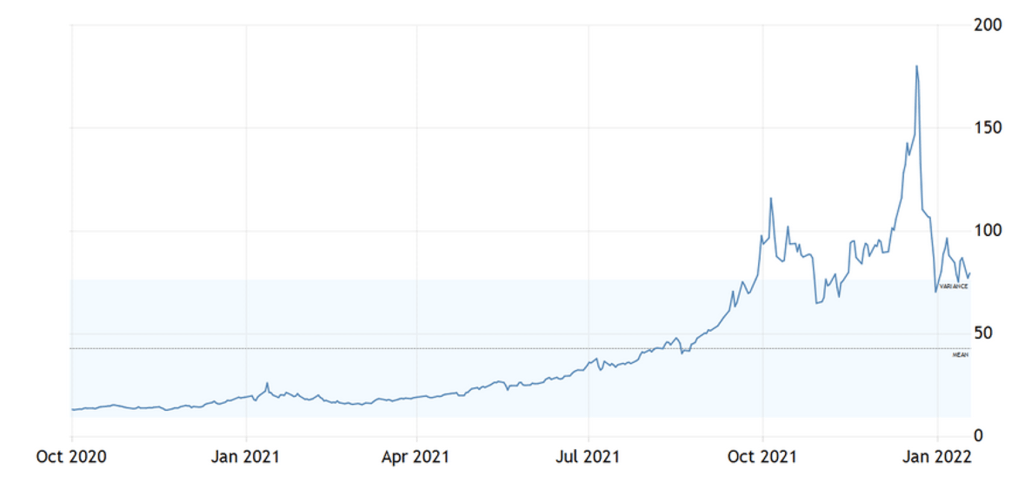

In the last six months, Europe has been hit by a natural gas crisis with a severe surge in prices. Politicians, industry representatives, and end-energy users voiced their discontent after a more than seven-fold price increase between May and December 2021 (see Figure 1). Even if gas prices somewhat stabilized this month (partly due to unusually warm weather), today, gas is four times as expensive as it was a year ago. This has already translated into an increase in electricity prices, and as a result, is also likely to have dramatic consequences for the cost and price of manufacturing goods.

Figure 1. Evolution of EU gas prices since Oct 2020.

Source: tradingeconomics.com

These ever-high gas prices have triggered legitimate concerns regarding the security of gas supply to Europe, specifically, driven by the dependency on Russian gas imports. Around 90% of EU natural gas is imported from outside the EU, and Russia is the largest supplier. In 2020, Russia provided nearly 44% of all EU gas imports, more than twice the second-largest supplier, Norway (19.9%, see Eurostat). The concern about Russian gas dependency was exacerbated by the new underwater gas route project connecting Russia and the EU – Nord Stream 2. The opponents to this new route argued that it will not only increase the EU’s gas dependency but also Russia’s political influence in the EU and its bargaining power against Ukraine (see, e.g., FT). Former President of the European Council Donald Tusk stated that “from the perspective of EU interests, Nord Stream 2 is a bad project.”.

However, neither dependency nor controversial gas route projects are a new phenomenon, and the EU has implemented some measures to tackle these issues in the past. This brief looks at the current security of Russian gas supply through the lens of these historical developments. We provide a snapshot of the risks associated with Russian gas imports faced by the EU a decade ago. We then discuss whether different factors affecting the EU gas supply security have changed since (and to which extent it may have contributed to the current situation) and if decreasing dependence on Russian gas is feasible and cost-effective. We conclude by addressing the policy implications.

Security of Russian Gas Supply to the EU, an Old Problem Difficult to Tackle

Russia has been the main gas provider to the EU for a few decades, and for a while, this dependency has triggered concerns about gas supply security (see, e.g., Stern, 2002 or Lewis, New York Times, 1982). However, the problem with the security of Russian gas supplies was extending beyond the dependency on Russian gas per se. It was driven by a range of risk factors such as insufficient diversification of gas suppliers, low fungibility of natural gas supplies with a prevalence of pipeline gas delivery, or use of gas exports/transit as means to solve geopolitical problems.

This last point became especially prominent in the mid-to-late-2000s, during the “gas wars” between Russia and the gas transit countries Ukraine and Belarus. These wars led to shortages and even a complete halt of Russian gas delivery to some EU countries, showing how weak the security of the Russian gas supply to the EU was at that time.

Reacting to these “gas wars”, the EU attempted to tackle the issue with a revival of the “common energy policy” based on the “solidarity” and “speaking in one voice” principles. The EU wanted to adopt a “coherent approach in the energy relations with third countries and an internal coordination so that the EU and its Member States act together” (see, e.g., EC, 2011). However, this idea turned out to be challenging to implement, primarily because of one crucial contributor to the problem with the security of Russian gas supply – the sizable disbalance in Russian gas supply risk among the individual EU Member States.

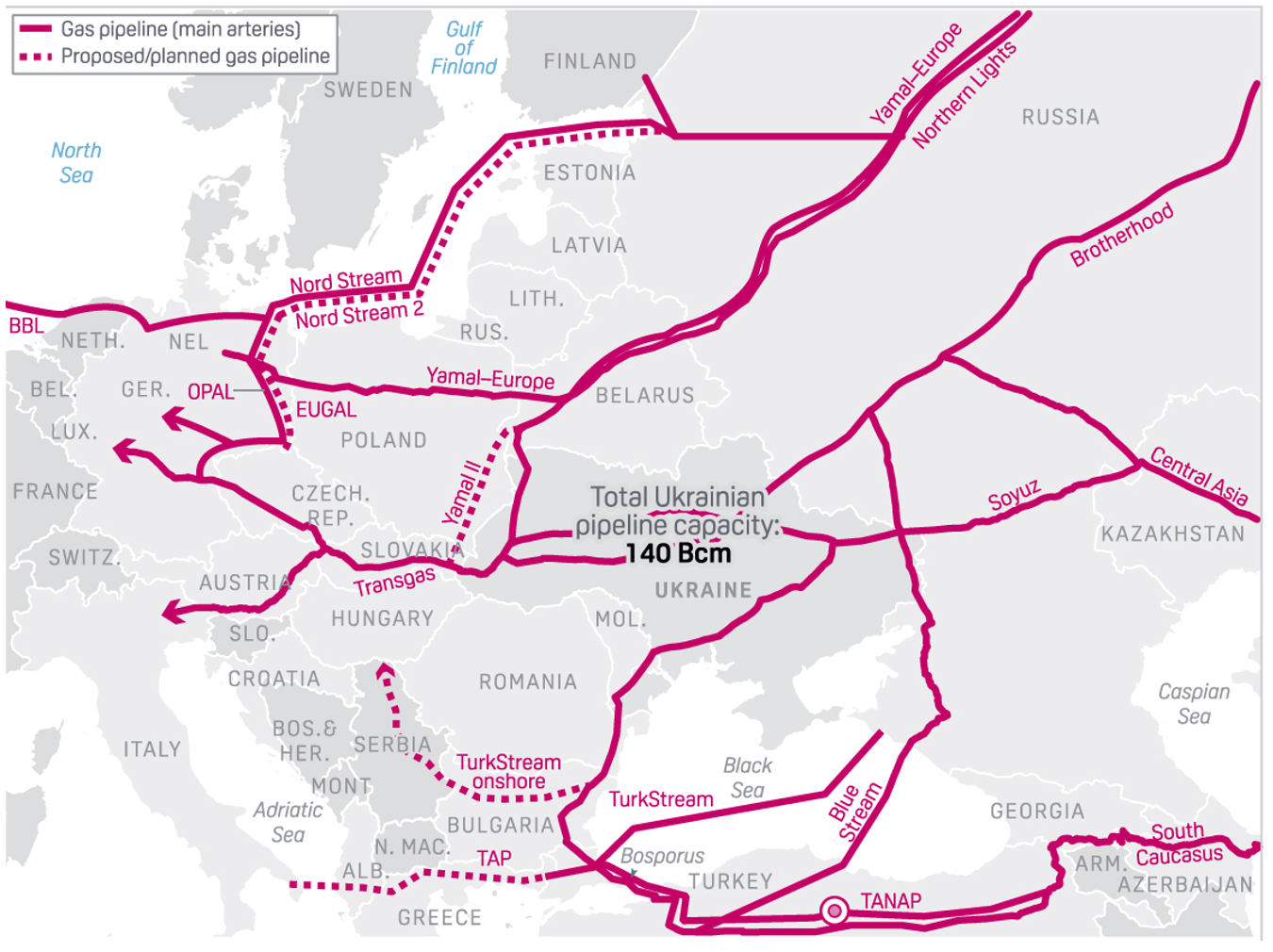

Indeed, EU Member States had a different share of natural gas in their total energy consumption, highly uneven diversification of gas suppliers, and varying exposure to Russian gas. Several Eastern-European EU states (such as Bulgaria, Estonia, or Czech Republic) were importing their gas almost entirely from Russia; other EU Member States (such as Germany, Italy, or Belgium) had a diversified gas import portfolio; and a few EU states (e.g., Spain or Portugal) were not consuming any Russian gas at all. Russian natural gas was delivered via several routes (see Figure 2), and member states were using different transit routes and facing different transit-associated risks. These differences naturally led to misalignment of energy policy preferences across EU states, creating policy tensions and making it difficult to implement a common energy policy with “speaking in one voice” (see more on this issue in Le Coq and Paltseva, 2009 and 2012).

Figure 2. Gas pipeline in Europe.

Source: S&G Platt.

The introduction of Nord Stream 1 in 2011 is an excellent example of the problem’s complexity. This new gas transit route from Russia increased the reliability of Russian gas supply for EU countries connected to this route (like Germany or France), as they were able to better diversify the transit of their imports from Russia and be less exposed to transit risks. The “Nord Stream” countries (i.e., countries connected to this route) were then willing to push politically and economically for this new project. Le Coq and Paltseva (2012) show, however, that countries unconnected to this new route while simultaneously sharing existing, “older” routes with “Nord Stream” countries would experience a decrease in their gas supply security. The reason for this is that the “directly connected” countries would now be less interested in exerting “common” political pressure to secure gas supplies along the “old” routes.

This is not to say that the EU did not learn from the above lessons. While the “speaking in one voice” energy policy initiative was not entirely successful, the EU has implemented a range of actions to cope with the risks of the security of gas supply from Russia. The next section explains how the situation is has changed since, outlining both the progress made by the EU and the newly arising risk factors.

Security of Russian Gas Supply to the EU, a Current Problem Partially Addressed

Since the end of the 2000s, the EU implemented a few changes that have positively affected the security of gas supply from Russia.

First, the EU put a significant effort into developing the internal gas market, altering both the physical infrastructure and the gas market organization. The EU updated and extended the internal gas network and introduced the wide-scale possibility of utilizing reverse flow, effectively allowing gas pipelines to be bi- rather than uni-directional. These actions improved the gas interconnections between the EU states (and other countries), thereby making potential disruptions along a particular gas transit route less damaging and diminishing the asymmetry of exposure to route-specific gas transit risks among the EU members. Ukraine’s gas import situation is a good illustration of the effect of reverse flow. Ukraine does not directly import Russian gas since 2016, mainly from Slovakia (64%), Hungary (26%), and Poland (10%) (see here). The transformation of the gas market organization brought about the implementation of a natural gas hub in Europe and change in the mechanism of gas price formation. It is now possible to buy and sell natural gas via long-term contracts and on the spot market. With the gas market becoming more liquid, it became easier to prevent the gas supply disruption threat.

Second, Europe has made certain progress in diversifying its gas exports. According to Komlev (2021), the concentration of EU gas imports from outside of the EU (excluding Norway), as measured by the Herfindahl-Hirschman index, has decreased by around 25% between 2016 and 2020. While the imports are still highly concentrated, with the HHI equal to 3120 in 2020, this is a significant achievement. A large part of this diversification effort is the dramatic increase in the share of liquified natural gas (i.e., LNG) in its gas imports – in 2020, a fair quarter of the EU gas imports came in the form of LNG. An expanded capacity for LNG liquefaction and better fungibility of LNG would facilitate backup opportunities in the case of Russian gas supply risks and improve the diversification of the EU gas imports, thereby increasing the security of natural gas supply.

However, the above developments also have certain disadvantages, which became especially prominent during the ongoing gas crisis. For example, the fungibility of LNG has a reverse side: LNG supplies respond to variations in gas market prices across the world. This change has intensified the competition on the demand side – Europe and Asia might now compete for the same LNG. This is likely to make a secure supply of LNG – e.g., as a backup in the case of a gas supply default or as a diversification device – a costly option.

In turn, new mechanisms of gas price formation in Europe included decoupling the oil and gas prices and changing the format of long-term gas contracts. The percentage of oil-linked contracts in gas imports to the EU dropped from 47% in 2016 to 26% in 2020. In particular, 87% of Gazprom’s long-term contracts in 2020 were linked to spot and forward gas prices and only around 13% to oil prices (Komlev, 2021). This gas-on-gas linking may have contributed to the current gas crisis: Indeed, it undermined the economic incentives of Gazprom to supply more gas to the EU spot market in the current high-price market. Shipping more gas would lower spot prices and prices of hub-linked longer-term contracts for Gazprom. In that sense, the ongoing decline in Russian gas supplies to the EU may reflect not (only) geopolitical considerations but economic optimization.

Similarly, this new mechanism also finds reflection in the ongoing situation with the EU gas storage. The current EU storage capacity is 117 bcm, or almost 20% of its yearly consumption, and thus, can in principle be effective in managing the short-term volume and price shocks. However, the current gas crisis has shown that this option might be far from sufficient in the case of a gas shortage (see, e.g., Zachmann et al., 2021). One of the reasons for this insufficiency can be Gazprom controlling a sizable share of this storage capacity (see here). For example, Gazprom owns (directly and indirectly) almost one-third of all gas storage in Germany, Austria, and the Netherlands. Combining this storage market position with a long-term gas contract structure may also lead to strategic behavior for economic (on top of potential political) purposes.

Last but not least, the EU gas market is likely to be characterized by increased demand due to the green transition agenda (see Olofsgård and Strömberg, 2022). Being the least carbon-intensive fossil fuel, natural gas has an important role in facilitating green transition and increasing the electrification of the economy. For example, Le Coq et al. (2018) argues that gas capacity should be around 3 to 4 times the current capacity by 2050 for full electrification of transport and heating in France, Germany, or the Netherlands. In such circumstances, the EU is not likely to have the luxury to diminish reliance on Russian gas.

Conclusions and Policy Implications

Keeping the above discussion in mind, should the EU try to diminish its dependence on Russian gas to improve its energy security? This may be true in theory, but in practice, this might be too costly, at least in the short-to-medium run.

The current situation on the EU gas market suggests that simply cutting gas imports from Russia is likely to lead to high prices both in the energy sector and, later, in other sectors of the economy due to spillovers. Substituting gas imports from Russia with gas from other sources, such as LNG, is likely to be very costly and not necessarily very reliable. Alternative measures, e.g., improving interconnections between the EU Member States or controlling transit issues via the use of reverse flow technology, are effective but have limited impact. Simply cutting down gas demand is not a viable strategy. Indeed, with the EU pushing for a green transition and the electrification of the economy, the EU’s gas imports may have to increase. Russian gas may play an important role in this process.

As a result, we believe that the solution to keep the security issue of Russian gas supply at bay lies in the area of common energy policy. It is essential that the EU implements and effectively manages a coordinated approach in dealing with Russian gas supplies. The EU is the largest buyer of Russian gas, and given Russian dependency on hydrocarbon exports, such a synchronized approach would give the EU the possibility to exploit its “large buyer” power. While the asymmetry in exposure to Russian gas supply risks among the EU Member States is still sizable, the improvements in the functioning of the internal gas market and gas transportation within the EU make their preferences more aligned, and a common policy vector more feasible. Furthermore, recent EU initiatives on creating “strategic gas reserves” by making the Member States share their gas storage with one another would further facilitate such coordination. Implementing the “speaking in one voice” gas import policy will allow the EU to fully utilize its bargaining power vis-à-vis Gazprom and spread the benefits of new gas routes from Russia – such as Nord Stream 2 – across its Member States.

References

Disclaimer: Opinions expressed in events, policy briefs, working papers and other publications are those of the authors and/or speakers; they do not necessarily reflect those of SITE, the FREE Network and its research institutes.